THE BE YOUR OWN ECONOMIST ® BLOG

The Lehmann Letter ©

President-elect Obama is doing all he can to build confidence that his administration will hit the deck running on January 20, 2009. His economic team is in place and he has made clear that stimulating economic recovery, not deficit reduction or balancing the budget, is his first priority.

Good for him. Everyone wishes him well.

But the statistical news remains grim. Yesterday the Bureau of Economic Analysis (BEA) confirmed that GDP fell in the third quarter. The announcement also said (http://www.bea.gov/newsreleases/national/gdp/gdpnewsrelease.htm): “Profits from current production (corporate profits with inventory valuation and capital consumption adjustments) decreased $14.6 billion in the third quarter, compared with a decrease of$60.2 billion in the second quarter.” As a matter of fact, corporate profits were lower than at any time since the fourth quarter of 2005, almost three years ago.

The BEA also reported that consumption expenditures dropped by one percent in October (http://www.bea.gov/newsreleases/national/pi/pinewsrelease.htm): “Personal income increased $42.4 billion, or 0.3 percent, and disposable personal income (DPI) increased $45.1 billion, or 0.4 percent, in October, according to the Bureau of Economic Analysis. Personal consumption expenditures (PCE) decreased $102.8 billion, or 1.0 percent.” Despite income growth, consumers reduced spending. That’s a clear sign of the fear and uncertainty that grips households. They’d rather build their balance sheets than spend their income.

Today the Census Bureau released new-home sales data for October (http://www.census.gov/const/newressales.pdf): “Sales of new one-family houses in October 2008 were at a seasonally adjusted annual rate of 433,000, according to estimates released jointly today by the U.S. Census Bureau and the Department of Housing and Urban Development. This is 5.3 percent (±15.0%)* below the revised September of 457,000 and is 40.1 percent (±9.9%) below the October 2007 estimate of 723,000.”

Home sales are 40% below last year’s level and about a low as they were in the 1900-91 recession. Almost 20 years of gains are gone.

The Census Bureau also reported (http://www.census.gov/indicator/www/m3/adv/pdf/durgd.pdf): “New orders for manufactured durable goods in October decreased $12.7 billion or 6.2 percent to $193.0 billion, the U.S. Census Bureau announced today. This was the largest percent decrease in new orders since October 2006 and followed two consecutive monthly decreases including a 0.2 percent September decrease…..Nondefense new orders for capital goods in October

decreased $2.4 billion or 3.6 percent to $65.6 billion.”

Durable-good manufacturing has stalled, especially new orders for nondefense capital goods. This is a leading indicator of business capital expenditures.

There you have it: Profits, consumer spending and business capital expenditures are all down sharply. The new president is doing what he can to instill confidence in the forthcoming administration, but he’s clearly swimming upstream.

© 2008 Michael B. Lehmann

Wednesday, November 26, 2008

Tuesday, November 25, 2008

A Step In The Right Direction

THE BE YOUR OWN ECONOMIST ® BLOG

The Lehmann Letter ©

Today the Fed announced two initiatives designed to hasten our emergence from the financial crisis (http://www.federalreserve.gov/newsevents/press/monetary/20081125a.htm and http://www.federalreserve.gov/newsevents/press/monetary/20081125b.htm.)

In the Fed’s own words:

“…the Term Asset-Backed Securities Loan Facility (TALF), (is) a facility that will help market participants meet the credit needs of households and small businesses by supporting the issuance of asset-backed securities (ABS) collateralized by student loans, auto loans, credit card loans, and loans guaranteed by the Small Business Administration (SBA).

“Under the TALF, the Federal Reserve Bank of New York (FRBNY) will lend up to $200 billion on a non-recourse basis to holders of certain AAA-rated ABS backed by newly and recently originated consumer and small business loans. The FRBNY will lend an amount equal to the market value of the ABS less a haircut and will be secured at all times by the ABS. The U.S. Treasury Department--under the Troubled Assets Relief Program (TARP) of the Emergency Economic Stabilization Act of 2008--will provide $20 billion of credit protection to the FRBNY in connection with the TALF….”

“New issuance of ABS declined precipitously in September and came to a halt in October. At the same time, interest rate spreads on AAA-rated tranches of ABS soared to levels well outside the range of historical experience, reflecting unusually high risk premiums. The ABS markets historically have funded a substantial share of consumer credit and SBA-guaranteed small business loans. Continued disruption of these markets could significantly limit the availability of credit to households and small businesses and thereby contribute to further weakening of U.S. economic activity. The TALF is designed to increase credit availability and support economic activity by facilitating renewed issuance of consumer and small business ABS at more normal interest rate spreads.”

In addition:

“The Federal Reserve … will initiate a program to purchase the direct obligations of housing-related government-sponsored enterprises (GSEs)--Fannie Mae, Freddie Mac, and the Federal Home Loan Banks--and mortgage-backed securities (MBS) backed by Fannie Mae, Freddie Mac, and Ginnie Mae. Spreads of rates on GSE debt and on GSE-guaranteed mortgages have widened appreciably of late. This action is being taken to reduce the cost and increase the availability of credit for the purchase of houses, which in turn should support housing markets and foster improved conditions in financial markets more generally…..”

The Fed, with the Treasury’s assistance, wants to boost household purchases of durable goods (by freeing consumer credit) and new homes (by freeing mortgage borrowing). These measures should help.

But note the dire conditions in the asset-backed and mortgage-backed securities markets as revealed by the following excerpts from the Fed’s press release:

“New issuance of ABS declined precipitously in September and came to a halt in October. At the same time, interest rate spreads on AAA-rated tranches of ABS soared to levels well outside the range of historical experience, reflecting unusually high risk premiums. ……….Spreads of rates on GSE debt and on GSE-guaranteed mortgages have widened appreciably of late.“

Will the Fed’s actions be sufficient? To what extent are households reducing their purchases of durable goods and homes because they can’t obtain credit and to what extent are households reducing their purchases because they want to protect their balance sheets? And what role does the ongoing collapse of home prices contribute to the crisis and households’ desire to protect their balance sheets?

Perhaps a general moratorium on home foreclosures and massive assistance to indebted homeowners, by attacking the root cause of the crisis (collapsing home values), is the requisite first step that must be taken before other measures can become fully effective.

© 2008 Michael B. Lehmann

The Lehmann Letter ©

Today the Fed announced two initiatives designed to hasten our emergence from the financial crisis (http://www.federalreserve.gov/newsevents/press/monetary/20081125a.htm and http://www.federalreserve.gov/newsevents/press/monetary/20081125b.htm.)

In the Fed’s own words:

“…the Term Asset-Backed Securities Loan Facility (TALF), (is) a facility that will help market participants meet the credit needs of households and small businesses by supporting the issuance of asset-backed securities (ABS) collateralized by student loans, auto loans, credit card loans, and loans guaranteed by the Small Business Administration (SBA).

“Under the TALF, the Federal Reserve Bank of New York (FRBNY) will lend up to $200 billion on a non-recourse basis to holders of certain AAA-rated ABS backed by newly and recently originated consumer and small business loans. The FRBNY will lend an amount equal to the market value of the ABS less a haircut and will be secured at all times by the ABS. The U.S. Treasury Department--under the Troubled Assets Relief Program (TARP) of the Emergency Economic Stabilization Act of 2008--will provide $20 billion of credit protection to the FRBNY in connection with the TALF….”

“New issuance of ABS declined precipitously in September and came to a halt in October. At the same time, interest rate spreads on AAA-rated tranches of ABS soared to levels well outside the range of historical experience, reflecting unusually high risk premiums. The ABS markets historically have funded a substantial share of consumer credit and SBA-guaranteed small business loans. Continued disruption of these markets could significantly limit the availability of credit to households and small businesses and thereby contribute to further weakening of U.S. economic activity. The TALF is designed to increase credit availability and support economic activity by facilitating renewed issuance of consumer and small business ABS at more normal interest rate spreads.”

In addition:

“The Federal Reserve … will initiate a program to purchase the direct obligations of housing-related government-sponsored enterprises (GSEs)--Fannie Mae, Freddie Mac, and the Federal Home Loan Banks--and mortgage-backed securities (MBS) backed by Fannie Mae, Freddie Mac, and Ginnie Mae. Spreads of rates on GSE debt and on GSE-guaranteed mortgages have widened appreciably of late. This action is being taken to reduce the cost and increase the availability of credit for the purchase of houses, which in turn should support housing markets and foster improved conditions in financial markets more generally…..”

The Fed, with the Treasury’s assistance, wants to boost household purchases of durable goods (by freeing consumer credit) and new homes (by freeing mortgage borrowing). These measures should help.

But note the dire conditions in the asset-backed and mortgage-backed securities markets as revealed by the following excerpts from the Fed’s press release:

“New issuance of ABS declined precipitously in September and came to a halt in October. At the same time, interest rate spreads on AAA-rated tranches of ABS soared to levels well outside the range of historical experience, reflecting unusually high risk premiums. ……….Spreads of rates on GSE debt and on GSE-guaranteed mortgages have widened appreciably of late.“

Will the Fed’s actions be sufficient? To what extent are households reducing their purchases of durable goods and homes because they can’t obtain credit and to what extent are households reducing their purchases because they want to protect their balance sheets? And what role does the ongoing collapse of home prices contribute to the crisis and households’ desire to protect their balance sheets?

Perhaps a general moratorium on home foreclosures and massive assistance to indebted homeowners, by attacking the root cause of the crisis (collapsing home values), is the requisite first step that must be taken before other measures can become fully effective.

© 2008 Michael B. Lehmann

Monday, November 24, 2008

The New President’s Dilemma

THE BE YOUR OWN ECONOMIST ® BLOG

The Lehmann Letter ©

The Following Op-Ed ran in The San Francisco Chronicle on November 12 (http://www.sfgate.com/cgi-bin/article.cgi?f=/c/a/2008/11/12/EDLJ142NQS.DTL&hw=Michael+Lehmann&sn=001&sc=1000) . It’s still true.

President-elect Barack Obama faces a dilemma.

A severe recession is unfolding. Demand, production, employment, income - all are falling and falling hard. The new president has two traditional remedies at his disposal: Reduce taxes so that consumers can purchase more, thereby stimulating production and employment, or increase public-works spending to directly boost employment. These remedies will, of course, raise the federal deficit.

Therein lies the dilemma: The president cannot effectively deal with the recession and shrink the deficit. Which horn of the dilemma should the president choose?

In the spring of 1933, the same dilemma confronted President Franklin D. Roosevelt. FDR had campaigned on a balanced-budget platform. But when he took office, events left him no choice. FDR'S administration enacted sweeping measures that lifted federal spending and the federal deficit. The Works Progress Administration and the Civilian Conservation Corps spent billions on public works and employed millions. The deficit grew.

Obama now confronts the most serious economic crisis and dilemma since the Great Depression. Like FDR, he must choose between promoting economic recovery and containing the deficit. He can't do both.

The new president can use the $700 billion bank bailout as a template. In that instance, Congress moved decisively to meet the financial crisis. President Obama should present Congress with an equally large, bold and urgent program of tax cuts and spending increases to deal immediately with the recession. Households living from hand to mouth will spend any increase in after-tax income or extension of unemployment benefits. Now is the time to invest in the nation's crumbling infrastructure and the energy-independence and green-technology programs that Obama advocated.

The deficit will grow dramatically and the new administration should deal with it as soon as economic recovery is assured. Meanwhile, interest rates have fallen and the dollar has strengthened, proving that foreign investors remain willing to invest in America. If the rest of the world wants to invest in America, why shouldn't we? Recession confronts us immediately; national bankruptcy does not.

Now is not the time to think small.

© 2008 Michael B. Lehmann

The Lehmann Letter ©

The Following Op-Ed ran in The San Francisco Chronicle on November 12 (http://www.sfgate.com/cgi-bin/article.cgi?f=/c/a/2008/11/12/EDLJ142NQS.DTL&hw=Michael+Lehmann&sn=001&sc=1000) . It’s still true.

President-elect Barack Obama faces a dilemma.

A severe recession is unfolding. Demand, production, employment, income - all are falling and falling hard. The new president has two traditional remedies at his disposal: Reduce taxes so that consumers can purchase more, thereby stimulating production and employment, or increase public-works spending to directly boost employment. These remedies will, of course, raise the federal deficit.

Therein lies the dilemma: The president cannot effectively deal with the recession and shrink the deficit. Which horn of the dilemma should the president choose?

In the spring of 1933, the same dilemma confronted President Franklin D. Roosevelt. FDR had campaigned on a balanced-budget platform. But when he took office, events left him no choice. FDR'S administration enacted sweeping measures that lifted federal spending and the federal deficit. The Works Progress Administration and the Civilian Conservation Corps spent billions on public works and employed millions. The deficit grew.

Obama now confronts the most serious economic crisis and dilemma since the Great Depression. Like FDR, he must choose between promoting economic recovery and containing the deficit. He can't do both.

The new president can use the $700 billion bank bailout as a template. In that instance, Congress moved decisively to meet the financial crisis. President Obama should present Congress with an equally large, bold and urgent program of tax cuts and spending increases to deal immediately with the recession. Households living from hand to mouth will spend any increase in after-tax income or extension of unemployment benefits. Now is the time to invest in the nation's crumbling infrastructure and the energy-independence and green-technology programs that Obama advocated.

The deficit will grow dramatically and the new administration should deal with it as soon as economic recovery is assured. Meanwhile, interest rates have fallen and the dollar has strengthened, proving that foreign investors remain willing to invest in America. If the rest of the world wants to invest in America, why shouldn't we? Recession confronts us immediately; national bankruptcy does not.

Now is not the time to think small.

© 2008 Michael B. Lehmann

Tuesday, November 11, 2008

Taking A Break

THE BE YOUR OWN ECONOMIST ® BLOG

The Lehmann Letter ©

The blogger will take a brief respite and return on or about November 19.

© 2008 Michael B. Lehmann

The Lehmann Letter ©

The blogger will take a brief respite and return on or about November 19.

© 2008 Michael B. Lehmann

What About Homeowners?

THE BE YOUR OWN ECONOMIST ® BLOG

The Lehmann Letter ©

Every day we learn the government bailout has been extended to more businesses or there’s an effort under way to broaden the bailout’s coverage.

The banks are gobbling up their share of the $700 billion package. AIG’s assistance has topped $100 billion. The automakers will probably receive a rescue package. American Express has obtained permission to become a bank in order to ease the strains facing its credit-card business.

Meanwhile, home prices continue to plunge as foreclosures grow. Millions will lose their homes and millions more will end up under water (mortgage debt exceeds home’s value). What’s fair about that? Why should homeowners suffer while financial institutions and manufacturers are thrown a life line?

Everyone knows what needs to be done. There should be an immediate 90-day moratorium on foreclosures. During that period mortgages should be written down to the property’s market value for those homeowners who can’t make their payments. This entails a means test, so one should be created. If the homeowner still can’t pay the mortgage, then the term of the loan should be extended and the interest rate reduced. The federal government can compensate the lender for any loss.

That would direct relief to those who need it most.

Would there be complaints by those not facing foreclosure because the means test demonstrated their ability to pay? Would they be jealous of those who received assistance when they did not? Perhaps. But it would still be worth it to stop the losses and halt the foreclosures.

Would prices stop falling? Probably not. But they would not fall as far as they will fall if we don’t stop the foreclosures.

Washington should stop thinking small!

© 2008 Michael B. Lehmann

The Lehmann Letter ©

Every day we learn the government bailout has been extended to more businesses or there’s an effort under way to broaden the bailout’s coverage.

The banks are gobbling up their share of the $700 billion package. AIG’s assistance has topped $100 billion. The automakers will probably receive a rescue package. American Express has obtained permission to become a bank in order to ease the strains facing its credit-card business.

Meanwhile, home prices continue to plunge as foreclosures grow. Millions will lose their homes and millions more will end up under water (mortgage debt exceeds home’s value). What’s fair about that? Why should homeowners suffer while financial institutions and manufacturers are thrown a life line?

Everyone knows what needs to be done. There should be an immediate 90-day moratorium on foreclosures. During that period mortgages should be written down to the property’s market value for those homeowners who can’t make their payments. This entails a means test, so one should be created. If the homeowner still can’t pay the mortgage, then the term of the loan should be extended and the interest rate reduced. The federal government can compensate the lender for any loss.

That would direct relief to those who need it most.

Would there be complaints by those not facing foreclosure because the means test demonstrated their ability to pay? Would they be jealous of those who received assistance when they did not? Perhaps. But it would still be worth it to stop the losses and halt the foreclosures.

Would prices stop falling? Probably not. But they would not fall as far as they will fall if we don’t stop the foreclosures.

Washington should stop thinking small!

© 2008 Michael B. Lehmann

Friday, November 7, 2008

Minus 1.2 Million, And Counting

THE BE YOUR OWN ECONOMIST ® BLOG

The Lehmann Letter ©

This morning’s employment report was remarkable (http://stats.bls.gov/news.release/empsit.nr0.htm). It began:

“Nonfarm payroll employment fell by 240,000 in October, and the unemployment rate rose from 6.1 to 6.5 percent, the Bureau of Labor Statistics of the U.S. Department of Labor reported today. October's drop in payroll employment followed declines of 127,000 in August and 284,000 in September, as revised. Employment has fallen by 1.2 million in the first 10 months of 2008; over half of the decrease has occurred in the past 3 months. In October, job losses continued in manufacturing, construction, and several service-providing industries. Health care and mining continued to add jobs.”

We lost 240,000 jobs last month and September’s loss was revised upward to 284,000. Moreover, we’ve lost 1.2 million jobs this year, for an average monthly loss of 120,000. That’s awful.

If you update the chart below in your mind’s eye, you can see that the recent monthly losses of 284,000 and 240,000 are as bad as the 2001 dot-com recession. And all signs seem to say: The worst is yet to come.

Job Growth

(Click on chart to enlarge)

© 2008 Michael B. Lehmann

The Lehmann Letter ©

This morning’s employment report was remarkable (http://stats.bls.gov/news.release/empsit.nr0.htm). It began:

“Nonfarm payroll employment fell by 240,000 in October, and the unemployment rate rose from 6.1 to 6.5 percent, the Bureau of Labor Statistics of the U.S. Department of Labor reported today. October's drop in payroll employment followed declines of 127,000 in August and 284,000 in September, as revised. Employment has fallen by 1.2 million in the first 10 months of 2008; over half of the decrease has occurred in the past 3 months. In October, job losses continued in manufacturing, construction, and several service-providing industries. Health care and mining continued to add jobs.”

We lost 240,000 jobs last month and September’s loss was revised upward to 284,000. Moreover, we’ve lost 1.2 million jobs this year, for an average monthly loss of 120,000. That’s awful.

If you update the chart below in your mind’s eye, you can see that the recent monthly losses of 284,000 and 240,000 are as bad as the 2001 dot-com recession. And all signs seem to say: The worst is yet to come.

Job Growth

(Click on chart to enlarge)

Recessions shaded

The chart was taken from http://www.beyourowneconomist.com. [Click on Seminars and then Charts.] Go there for additional charts on the economy and a list of economic indicators.)

The chart was taken from http://www.beyourowneconomist.com. [Click on Seminars and then Charts.] Go there for additional charts on the economy and a list of economic indicators.)

© 2008 Michael B. Lehmann

Wednesday, November 5, 2008

The New President’s Dilemma

THE BE YOUR OWN ECONOMIST ® BLOG

The Lehmann Letter ©

President-elect Barack Obama faces a dilemma.

A severe recession is unfolding. Demand, production, employment, income – all are falling and falling hard. The new president has two traditional remedies at his disposal: Reduce taxes so that consumers can purchase more, thereby stimulating production and employment, or increase public-works spending to directly boost employment. These remedies will, of course, raise the federal deficit.

Therein lies the dilemma: The president can not effectively deal with the recession and shrink the deficit. Which horn of the dilemma should the president choose? Fight the recession or deal with the deficit?

In the spring of 1933 the same dilemma confronted President Roosevelt. FDR had campaigned on a balanced-budget platform. But when he took office, current events left him no choice. FDR’S administration enacted sweeping measures that lifted federal spending and the federal deficit. The Works Progress Administration and the Civilian Conservation Corps spent billions on public works and employed millions. The deficit grew.

Barack Obama now confronts the most serious economic crisis and dilemma since the Great Depression. Like FDR he must choose between promoting economic recovery and containing the deficit. He can’t do both.

The new president can use the $700 billion bank bailout as a template. In that instance Congress moved decisively to meet the financial crisis. President Obama should present Congress with an equally large, bold and urgent program of tax cuts and spending increases to deal immediately with the recession. Households living from hand to mouth will spend any increase in after-tax income or extension of unemployment benefits. Now is the time to invest in the nation’s crumbling infrastructure and the energy-independence and green-technology programs that Mr. Obama advocated.

The deficit will grow dramatically and the new administration should deal with it as soon as economic recovery is assured. Meanwhile, interest rates have fallen and the dollar has strengthened, proving that foreign investors remain willing to purchase Treasury securities. Recession confronts us immediately; national bankruptcy does not.

Now is not the time to think small.

© 2008 Michael B. Lehmann

The Lehmann Letter ©

President-elect Barack Obama faces a dilemma.

A severe recession is unfolding. Demand, production, employment, income – all are falling and falling hard. The new president has two traditional remedies at his disposal: Reduce taxes so that consumers can purchase more, thereby stimulating production and employment, or increase public-works spending to directly boost employment. These remedies will, of course, raise the federal deficit.

Therein lies the dilemma: The president can not effectively deal with the recession and shrink the deficit. Which horn of the dilemma should the president choose? Fight the recession or deal with the deficit?

In the spring of 1933 the same dilemma confronted President Roosevelt. FDR had campaigned on a balanced-budget platform. But when he took office, current events left him no choice. FDR’S administration enacted sweeping measures that lifted federal spending and the federal deficit. The Works Progress Administration and the Civilian Conservation Corps spent billions on public works and employed millions. The deficit grew.

Barack Obama now confronts the most serious economic crisis and dilemma since the Great Depression. Like FDR he must choose between promoting economic recovery and containing the deficit. He can’t do both.

The new president can use the $700 billion bank bailout as a template. In that instance Congress moved decisively to meet the financial crisis. President Obama should present Congress with an equally large, bold and urgent program of tax cuts and spending increases to deal immediately with the recession. Households living from hand to mouth will spend any increase in after-tax income or extension of unemployment benefits. Now is the time to invest in the nation’s crumbling infrastructure and the energy-independence and green-technology programs that Mr. Obama advocated.

The deficit will grow dramatically and the new administration should deal with it as soon as economic recovery is assured. Meanwhile, interest rates have fallen and the dollar has strengthened, proving that foreign investors remain willing to purchase Treasury securities. Recession confronts us immediately; national bankruptcy does not.

Now is not the time to think small.

© 2008 Michael B. Lehmann

Tuesday, November 4, 2008

10.5

THE BE YOUR OWN ECONOMIST ® BLOG

The Lehmann Letter ©

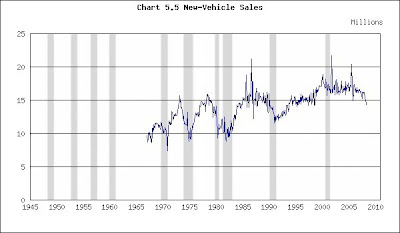

Everette P. Johnson at the Bureau of Economic Analysis has done a great job over the years maintaining the Bureau’s motor-vehicle-sales data base. The number for the previous month usually appears about the third or fourth of the current month. So there’s little delay.

Here’s how to obtain the data.

Step 1: Go to http://www.bea.gov/

Step 1: Click on "Gross Domestic Product" under "National"

Step 2: Scroll down and click on "Motor Vehicles" under "Supplemental Estimates"

Step 3: Save to your desktop as an Excel file and then open the file

Step 4: Click on the "Table 6" tab at the bottom of the page

Step 5: Look at column I (Light Total) and scroll down for the latest data

You can see that 10.5 million vehicles sold in October 2008 at a seasonally-adjusted annual rate.

Put that figure in perspective by reviewing the data over the past year.

2007

October .............16.0

November..........16.0

December...........16.0

2008

January..............15.3

February............15.3

March.................15.0

April...................14.5

May....................14.2

June...................13.6

July....................12.5

August................13.7

September..........12.5

October..............10.5

Sales were falling before the financial crisis. Then they began to collapse.

Now examine the chart for historical perspective, updating it in your mind’s eye with the 10.5 October total.

New-Vehicle Sales

(Click on chart to enlarge)

© 2008 Michael B. Lehmann

The Lehmann Letter ©

Everette P. Johnson at the Bureau of Economic Analysis has done a great job over the years maintaining the Bureau’s motor-vehicle-sales data base. The number for the previous month usually appears about the third or fourth of the current month. So there’s little delay.

Here’s how to obtain the data.

Step 1: Go to http://www.bea.gov/

Step 1: Click on "Gross Domestic Product" under "National"

Step 2: Scroll down and click on "Motor Vehicles" under "Supplemental Estimates"

Step 3: Save to your desktop as an Excel file and then open the file

Step 4: Click on the "Table 6" tab at the bottom of the page

Step 5: Look at column I (Light Total) and scroll down for the latest data

You can see that 10.5 million vehicles sold in October 2008 at a seasonally-adjusted annual rate.

Put that figure in perspective by reviewing the data over the past year.

2007

October .............16.0

November..........16.0

December...........16.0

2008

January..............15.3

February............15.3

March.................15.0

April...................14.5

May....................14.2

June...................13.6

July....................12.5

August................13.7

September..........12.5

October..............10.5

Sales were falling before the financial crisis. Then they began to collapse.

Now examine the chart for historical perspective, updating it in your mind’s eye with the 10.5 October total.

New-Vehicle Sales

(Click on chart to enlarge)

Recessions shaded

You can see that auto sales did not suffer in the 2001 recession. Falling interest rates kept them afloat, just as they buoyed residential real estate.

Nor did auto sales fall below 12 million in the 1990-91 recession.

We have to go back to1981-82 and earlier recessions for numbers that fleetingly dip below 10 million.

The most recent data and the swiftness of its plunge portend real disaster for the industry. Will sales drop below 10 million? If so, how far? What can save the industry? Falling fuel prices? Falling interest rates? Smaller vehicles? Maybe, maybe and maybe.

Then we’re reminded of consumer confidence’s October reading – 38 – and that further dampens hope (http://beyourowneconomist.blogspot.com/2008/10/blue-christmas.html) because consumer confidence is at a post-WWII low. Why should consumers buy when they feel so miserable?

Now think of all those industries dependant upon motor-vehicle sales: steel, glass, rubber tires, fuzzy dice.

It’s not good.

(The chart was taken from http://www.beyourowneconomist.com. [Click on Seminars and then Charts.] Go there for additional charts on the economy and a list of economic indicators.)

You can see that auto sales did not suffer in the 2001 recession. Falling interest rates kept them afloat, just as they buoyed residential real estate.

Nor did auto sales fall below 12 million in the 1990-91 recession.

We have to go back to1981-82 and earlier recessions for numbers that fleetingly dip below 10 million.

The most recent data and the swiftness of its plunge portend real disaster for the industry. Will sales drop below 10 million? If so, how far? What can save the industry? Falling fuel prices? Falling interest rates? Smaller vehicles? Maybe, maybe and maybe.

Then we’re reminded of consumer confidence’s October reading – 38 – and that further dampens hope (http://beyourowneconomist.blogspot.com/2008/10/blue-christmas.html) because consumer confidence is at a post-WWII low. Why should consumers buy when they feel so miserable?

Now think of all those industries dependant upon motor-vehicle sales: steel, glass, rubber tires, fuzzy dice.

It’s not good.

(The chart was taken from http://www.beyourowneconomist.com. [Click on Seminars and then Charts.] Go there for additional charts on the economy and a list of economic indicators.)

© 2008 Michael B. Lehmann

Monday, November 3, 2008

Another Bad Number

THE BE YOUR OWN ECONOMIST ® BLOG

The Lehmann Letter ©

Today the Institute for Supply Management reported its October Purchasing Managers’ Index at 38.9 (http://www.ism.ws/ISMReport/MfgROB.cfm?navItemNumber=12942).

Norbert J. Ore, the Institute’s chair, said: "The PMI indicates a significantly faster rate of decline in manufacturing when comparing October to September. It appears that manufacturing is experiencing significant demand destruction as a result of recent events, with members indicating challenges associated with the financial crisis, interruptions from the Gulf hurricane, and the lagging impact from higher oil prices. This is the lowest level for the PMI since September 1982 when it registered 38.8 percent. In this report, we see inflationary pressures dissolving as the Prices Index fell to 37 percent, the lowest since December 2001 when it registered 33.2 percent. Export orders also contracted for the first time following 70 months of growth."

Pay attention: ‘….. significantly faster rate of decline...,” “ significant demand destruction…,” “…”inflationary pressures dissolving…,” “…Export orders also contracted for the first time following 70 months of growth."

And then look again at that number – 38.9 – and use it to update the chart.

Purchasing Managers’ Index

(Click on chart to enlarge)

The Lehmann Letter ©

Today the Institute for Supply Management reported its October Purchasing Managers’ Index at 38.9 (http://www.ism.ws/ISMReport/MfgROB.cfm?navItemNumber=12942).

Norbert J. Ore, the Institute’s chair, said: "The PMI indicates a significantly faster rate of decline in manufacturing when comparing October to September. It appears that manufacturing is experiencing significant demand destruction as a result of recent events, with members indicating challenges associated with the financial crisis, interruptions from the Gulf hurricane, and the lagging impact from higher oil prices. This is the lowest level for the PMI since September 1982 when it registered 38.8 percent. In this report, we see inflationary pressures dissolving as the Prices Index fell to 37 percent, the lowest since December 2001 when it registered 33.2 percent. Export orders also contracted for the first time following 70 months of growth."

Pay attention: ‘….. significantly faster rate of decline...,” “ significant demand destruction…,” “…”inflationary pressures dissolving…,” “…Export orders also contracted for the first time following 70 months of growth."

And then look again at that number – 38.9 – and use it to update the chart.

Purchasing Managers’ Index

(Click on chart to enlarge)

Recessions shaded

We’re down to levels not seen since the 1981-82 recession. That’s bad.

But it will get worse. Manufacturing has only just begun its hard contraction. So far it’s been slipping. Now the sliding starts. As purchases of consumer durables (think autos) and nondurables (such as apparel) plunge in the fourth quarter, manufacturing activity will shrink.

How do we know? Check out the October 28 blog, Blue Christmas, at http://beyourowneconomist.blogspot.com/2008/10/blue-christmas.html.

Consumer confidence has fallen to its lowest recorded post-WWII level. Consumers won’t spend under those conditions, and manufacturers’ markets will consequently dry up.

And why should businesses invest in new capacity under these circumstances? That’s another weak spot for manufacturing.

Then scroll back up to see what Mr. Ore said about exports: “…Export orders also contracted for the first time following 70 months of growth." The rest of the world can’t buy our goods when their economies are shrinking and the dollar is stronger.

Finally, what about Mr. Ore’s comment that “…”inflationary pressures (are) dissolving….” Isn’t that a silver lining? Sorry, that’s just further confirmation that demand is weak.

The bottom line: Things are bad and getting worse.

(The chart was taken from http://www.beyourowneconomist.com. [Click on Seminars and then Charts.] Go there for additional charts on the economy and a list of economic indicators.)

© 2008 Michael B. Lehmann

November Publication Schedule & Web Sources

THE BE YOUR OWN ECONOMIST ® BLOG

The Lehmann Letter ©

You can use the WEB SOURCES listing (below) to find the data on your own and read the accompanying press release. The addresses take you to the source’s home page and the steps tell you how to navigate the site. That way (rather than provide a direct link to the data) you can become familiar with these sites and find additional information on your own.

PUBLICATION SCHEDULE

November 2008

Source (* below)…………Series Description…………Day & Date

Quarterly Data

BLS………………….Productivity………………………….Thu, 6th

BEA…………………………GDP……………………...……Tue, 25th

Monthly Data

ISM………………….Purchasing managers’ index……….Mon, 3rd

Fed…………………………..Consumer credit……..……….Fri, 7th

BLS………………………….Employment………………… Fri, 7th

Census……………………...Balance of trade………………Thu, 13th

Census……………………...Retail trade…………………….Fri, 14th

Census……………………...Inventories……………………..Fri, 14th

Fed…………………………..Industrial production………….Mon, 17th

Fed………………………….Capacity utilization…………….Mon, 17th

BLS………………………….Producer prices……………….Tue, 18th

BLS………………………….Consumer prices……………...Wed, 19th

Census……………………..Housing starts………………….Wed, 19th

Conf Bd…………………….Leading Indicators…………….Thu, 20th

NAR…………………………Existing-home sales…….…….Mon, 24th

Conf Bd…………………….Consumer confidence…………Tue, 25th

Census…………………….Capital goods……………….…..Wed, 26th

Census……………………..New-home sales……………….Wed, 26th

* BEA = Bureau of Economic Analysis of the U.S. Department of Commerce

* BLS = Bureau of Labor Statistics of the U.S. Department of Labor

* Census = U.S. Bureau of the Census

* Conf Bd = Conference Board

* Fed = Federal Reserve System

* ISM = Institute for Supply Management

* NAR = National Association of Realtors

WEB SOURCES

Index of Leading Economic Indicators: http://www.conference-board.org/..........

Step 1: Click on "Economics" in the left-hand menu bar…………………………………….

Step 2: Click on "Economic Indicators" under "Economics" in the left-hand menu bar………………………………………………………………………………………………………………..

Step 3: Click on link under "U.S. Leading Indicators"………………………………………

Gross Domestic Product: http://www.bea.gov/....................................................

Step 1: Click on "Gross Domestic Product" under "National"………………………….

Step 2: Click on "National Income and Product Accounts Tables" under "Gross Domestic Product (GDP)"……………………………………………………………………………

Step 3: Click on "list of all NIPA Tables"………………………………………………………….

Step 4: Click on "Table 1.1.6. Real Gross Domestic Product..." and "Table 1.1.1. Percent Change

Step 5: Scroll down to line 1 in both tables and go to the last column on the right

Industrial Production & Capacity Utilization: http://www.federalreserve.gov/

Step 1: Click on "All Statistical Releases" under "Recent Statistical Releases" and then click on "Industrial Production and Capacity Utilization" under "Principal Economic Indicators" in the upper left…………………………………………………………

Step 2: Find the latest monthly data in the table next to "Total index" and "Total industry"……………………………………………………………………………………………………..

Institute For Supply Management Index: http://www.ism.ws/ ……………………….

Step 1: Click on "ISM Report on Business" in left-hand menu bar……………………

Step 2: Click on “Latest Manufacturing ROB” and find the latest PMI…………….

Producer Prices: http://stats.bls.gov/.....................................................................

Step 1: Click on “Producer Price Indexes” under “Inflation & Consumer Spending” in left-hand menu bar………………………………………………………………….

Step 2: Note "Finished goods" under "Latest Numbers" in upper right and multiply by 12 to put the data on an annual basis……………………………………….

Business Capital Expenditures (Nondefense Capital Goods): http://www.census.gov/

Step 1: Click on "Economic Indicators" in the lower right…………………………………

Step 2: Click on "PDF" on the left under "Advance Report on Durable Goods Manufacturers' Shipments and Orders"…………………………………………………………..

Step 3: Scroll down to Table 1 and find new orders for nondefense capital goods near the bottom……………………………………………………………………………………………..

Inventories, Sales & Inventory/Sales Ratio: http://www.census.gov/

Step 1: Click on "Economic Indicators" in the lower right…………………………………

Step 2: Click on "HTML" on the left under "Manufacturing and Trade Inventories and Sales" Step 3: Scroll down to Table 1 and subtract previous month's inventories from latest month's and multiply by 12 to obtain inventory change, and then obtain the most recent inventory/sales ratio……………………………………………………………………

Consumer Price Index: http://stats.bls.gov/...........................................................

Step 1: Click on “Consumer Price Index” under “Inflation & Consumer Spending” in left-hand menu bar………………………………………………………………………………….

Step 2: Note "CPI-U..." at the top under "Latest Numbers" in upper right and multiply "SA" by 12 to put the data on an annual basis…………………………………..

Employment Data (Total Non-farm Payroll Employment) (Unemployment Rate) (Manufacturing Workweek): http://stats.bls.gov/ ………………………………………..

Step 1: Click on “National Employment” under “Employment & Unemployment” in right-hand menu bar………………………………………………………………………………

Step 2: Click on (HTML) following “Employment Situation Summary” under "Economic News Releases"……………………………………………………………………….

Step 3: Click on “Employment Situation Summary” under “Table of Contents”

Step 4: Scroll down to Table A and find the unemployment rate for all workers in the latest month, the change in nonfarm employment in the last column and manufacturing hours of work for the latest month…………………………………………..

Personal Income: http://www.bea.gov/.....................................................................

Step 1: Click on "Gross Domestic Product" under "National"……………………………..

Step 2: Click on "National Income and Product Accounts Tables" under "Gross Domestic Product (GDP)"…………………………………………………………………………….

Step 3: Click on "list of all NIPA Tables"……………………………………………………….

Step 4: Click on "Table 2.6 Personal Income...."

Step 5: Scroll down to line 1…………………………………………………………………………..

Consumer Confidence: http://www.conference-board.org/....................................

Step 1: Click on the "Economics" in the left-hand menu bar……………………………….

Step 2: Click on "Economic Indicators" under "Economics" in the left-hand menu bar………………………………………………………………………………………………………………..

Step 3: Click on link under "Consumer Confidence Index"…………………………………

Consumer Credit: http://www.federalreserve.gov/...................................................

Step 1: Click on "All Statistical Releases" under "Recent Statistical Releases" and then click on "Consumer credit -- G19" under "Household Finance" in the upper right…………………………………………………………………………………………………………..

Step 2: Click on "Current Release"…………………………………………………………………

Step 3: Go to "Amount ... billions of dollars" and subtract previous month from current month & multiply by 12 to obtain seasonally adjusted dollar amount at annual rate………………………………………………………………………………………………..

Housing Starts: http://www.census.gov/..................................................................

Step 1: Click on "Economic Indicators" in the lower right………………………………….

Step 2: Click on "PDF" on the left under "Current Press Release" under "Housing Starts/Building Permits"………………………………………………………………………………..

Step 3: Scroll down to "Housing Starts"…………………………………………………………..

Home Sales (Existing-Home Sales): http://www.realtor.org/.................................

Step 1: Click on "Research" in the left-hand menu bar……………………………………….

Step 2: Find "Existing-Home Sales" under "Housing Indicators"……………………..

Home Sales (New-Home Sales): http://www.census.gov/.......................................

Step 1: Click on "Economic Indicators" in the lower right………………………………..

Step 2: Click on "PDF" on the left under "Current Press Release" under "New Home Sales"………………………………………………………………………………………………….

Retail Sales: http://www.census.gov/.......................................................................

Step 1: Click on "Economic Indicators" in the lower right…………………………………..

Step 2: Scroll down to "Advance Monthly Sales for Retail and Food Services" and click on "HTML" on the left under "Current Press Release"………………………………

© 2008 Michael B. Lehmann

The Lehmann Letter ©

You can use the WEB SOURCES listing (below) to find the data on your own and read the accompanying press release. The addresses take you to the source’s home page and the steps tell you how to navigate the site. That way (rather than provide a direct link to the data) you can become familiar with these sites and find additional information on your own.

PUBLICATION SCHEDULE

November 2008

Source (* below)…………Series Description…………Day & Date

Quarterly Data

BLS………………….Productivity………………………….Thu, 6th

BEA…………………………GDP……………………...……Tue, 25th

Monthly Data

ISM………………….Purchasing managers’ index……….Mon, 3rd

Fed…………………………..Consumer credit……..……….Fri, 7th

BLS………………………….Employment………………… Fri, 7th

Census……………………...Balance of trade………………Thu, 13th

Census……………………...Retail trade…………………….Fri, 14th

Census……………………...Inventories……………………..Fri, 14th

Fed…………………………..Industrial production………….Mon, 17th

Fed………………………….Capacity utilization…………….Mon, 17th

BLS………………………….Producer prices……………….Tue, 18th

BLS………………………….Consumer prices……………...Wed, 19th

Census……………………..Housing starts………………….Wed, 19th

Conf Bd…………………….Leading Indicators…………….Thu, 20th

NAR…………………………Existing-home sales…….…….Mon, 24th

Conf Bd…………………….Consumer confidence…………Tue, 25th

Census…………………….Capital goods……………….…..Wed, 26th

Census……………………..New-home sales……………….Wed, 26th

* BEA = Bureau of Economic Analysis of the U.S. Department of Commerce

* BLS = Bureau of Labor Statistics of the U.S. Department of Labor

* Census = U.S. Bureau of the Census

* Conf Bd = Conference Board

* Fed = Federal Reserve System

* ISM = Institute for Supply Management

* NAR = National Association of Realtors

WEB SOURCES

Index of Leading Economic Indicators: http://www.conference-board.org/..........

Step 1: Click on "Economics" in the left-hand menu bar…………………………………….

Step 2: Click on "Economic Indicators" under "Economics" in the left-hand menu bar………………………………………………………………………………………………………………..

Step 3: Click on link under "U.S. Leading Indicators"………………………………………

Gross Domestic Product: http://www.bea.gov/....................................................

Step 1: Click on "Gross Domestic Product" under "National"………………………….

Step 2: Click on "National Income and Product Accounts Tables" under "Gross Domestic Product (GDP)"……………………………………………………………………………

Step 3: Click on "list of all NIPA Tables"………………………………………………………….

Step 4: Click on "Table 1.1.6. Real Gross Domestic Product..." and "Table 1.1.1. Percent Change

Step 5: Scroll down to line 1 in both tables and go to the last column on the right

Industrial Production & Capacity Utilization: http://www.federalreserve.gov/

Step 1: Click on "All Statistical Releases" under "Recent Statistical Releases" and then click on "Industrial Production and Capacity Utilization" under "Principal Economic Indicators" in the upper left…………………………………………………………

Step 2: Find the latest monthly data in the table next to "Total index" and "Total industry"……………………………………………………………………………………………………..

Institute For Supply Management Index: http://www.ism.ws/ ……………………….

Step 1: Click on "ISM Report on Business" in left-hand menu bar……………………

Step 2: Click on “Latest Manufacturing ROB” and find the latest PMI…………….

Producer Prices: http://stats.bls.gov/.....................................................................

Step 1: Click on “Producer Price Indexes” under “Inflation & Consumer Spending” in left-hand menu bar………………………………………………………………….

Step 2: Note "Finished goods" under "Latest Numbers" in upper right and multiply by 12 to put the data on an annual basis……………………………………….

Business Capital Expenditures (Nondefense Capital Goods): http://www.census.gov/

Step 1: Click on "Economic Indicators" in the lower right…………………………………

Step 2: Click on "PDF" on the left under "Advance Report on Durable Goods Manufacturers' Shipments and Orders"…………………………………………………………..

Step 3: Scroll down to Table 1 and find new orders for nondefense capital goods near the bottom……………………………………………………………………………………………..

Inventories, Sales & Inventory/Sales Ratio: http://www.census.gov/

Step 1: Click on "Economic Indicators" in the lower right…………………………………

Step 2: Click on "HTML" on the left under "Manufacturing and Trade Inventories and Sales" Step 3: Scroll down to Table 1 and subtract previous month's inventories from latest month's and multiply by 12 to obtain inventory change, and then obtain the most recent inventory/sales ratio……………………………………………………………………

Consumer Price Index: http://stats.bls.gov/...........................................................

Step 1: Click on “Consumer Price Index” under “Inflation & Consumer Spending” in left-hand menu bar………………………………………………………………………………….

Step 2: Note "CPI-U..." at the top under "Latest Numbers" in upper right and multiply "SA" by 12 to put the data on an annual basis…………………………………..

Employment Data (Total Non-farm Payroll Employment) (Unemployment Rate) (Manufacturing Workweek): http://stats.bls.gov/ ………………………………………..

Step 1: Click on “National Employment” under “Employment & Unemployment” in right-hand menu bar………………………………………………………………………………

Step 2: Click on (HTML) following “Employment Situation Summary” under "Economic News Releases"……………………………………………………………………….

Step 3: Click on “Employment Situation Summary” under “Table of Contents”

Step 4: Scroll down to Table A and find the unemployment rate for all workers in the latest month, the change in nonfarm employment in the last column and manufacturing hours of work for the latest month…………………………………………..

Personal Income: http://www.bea.gov/.....................................................................

Step 1: Click on "Gross Domestic Product" under "National"……………………………..

Step 2: Click on "National Income and Product Accounts Tables" under "Gross Domestic Product (GDP)"…………………………………………………………………………….

Step 3: Click on "list of all NIPA Tables"……………………………………………………….

Step 4: Click on "Table 2.6 Personal Income...."

Step 5: Scroll down to line 1…………………………………………………………………………..

Consumer Confidence: http://www.conference-board.org/....................................

Step 1: Click on the "Economics" in the left-hand menu bar……………………………….

Step 2: Click on "Economic Indicators" under "Economics" in the left-hand menu bar………………………………………………………………………………………………………………..

Step 3: Click on link under "Consumer Confidence Index"…………………………………

Consumer Credit: http://www.federalreserve.gov/...................................................

Step 1: Click on "All Statistical Releases" under "Recent Statistical Releases" and then click on "Consumer credit -- G19" under "Household Finance" in the upper right…………………………………………………………………………………………………………..

Step 2: Click on "Current Release"…………………………………………………………………

Step 3: Go to "Amount ... billions of dollars" and subtract previous month from current month & multiply by 12 to obtain seasonally adjusted dollar amount at annual rate………………………………………………………………………………………………..

Housing Starts: http://www.census.gov/..................................................................

Step 1: Click on "Economic Indicators" in the lower right………………………………….

Step 2: Click on "PDF" on the left under "Current Press Release" under "Housing Starts/Building Permits"………………………………………………………………………………..

Step 3: Scroll down to "Housing Starts"…………………………………………………………..

Home Sales (Existing-Home Sales): http://www.realtor.org/.................................

Step 1: Click on "Research" in the left-hand menu bar……………………………………….

Step 2: Find "Existing-Home Sales" under "Housing Indicators"……………………..

Home Sales (New-Home Sales): http://www.census.gov/.......................................

Step 1: Click on "Economic Indicators" in the lower right………………………………..

Step 2: Click on "PDF" on the left under "Current Press Release" under "New Home Sales"………………………………………………………………………………………………….

Retail Sales: http://www.census.gov/.......................................................................

Step 1: Click on "Economic Indicators" in the lower right…………………………………..

Step 2: Scroll down to "Advance Monthly Sales for Retail and Food Services" and click on "HTML" on the left under "Current Press Release"………………………………

© 2008 Michael B. Lehmann

Subscribe to:

Posts (Atom)