The Lehmann Letter (C)

The blogger will return after the New Year.

Happy Holidays to one and all!

Thursday, December 18, 2008

Tuesday, December 16, 2008

Fed Funds Flattened

THE BE YOUR OWN ECONOMIST ® BLOG

The Lehmann Letter ©

Today the Federal Reserve reduced its federal-funds-rate target to between 0% and ¼%. You can read the Fed’s press release at:

http://www.federalreserve.gov/newsevents/press/monetary/20081216b.htm .

Direct your attention to these key passages:

“Since the Committee's last meeting, labor market conditions have deteriorated, and the available data indicate that consumer spending, business investment, and industrial production have declined. Financial markets remain quite strained and credit conditions tight. Overall, the outlook for economic activity has weakened further……

“The Federal Reserve will employ all available tools to promote the resumption of sustainable economic growth and to preserve price stability. In particular, the Committee anticipates that weak economic conditions are likely to warrant exceptionally low levels of the federal funds rate for some time…….. “

The patient is in intensive care and the Fed is administering its strongest medicine. Will it work?

We’ll see. The Fed’s efforts are certainly superior to maintaining high interest rates in the face of the economy’s collapse. But will rock-bottom interest rates actively promote recovery?

During the 2000-2002 dot-com bust the Fed also promoted interest-rates’ decline. Fortunately housing and autos responded favorably to these cuts, remained strong, and then blossomed by rising to sustained levels not seen before. Unfortunately we know how that story ended. Housing collapsed under its own bloated weight and dragged autos down with it. Falling interest rates have not yet resurrect these key sectors.

During earlier business cycles, in the 1960s and 1970s, a surging economy – booming housing and autos - ignited inflation and rising interest rates. Higher prices and higher borrowing costs choked-off the boom – slumping housing and autos - and led to recession. But these slumps were self-correcting because recession’s depressed conditions reduced inflation and interest rates, thereby reigniting – housing and autos - economic growth.

The economy behaved like a frisky horse in these earlier cycles, charging ahead when the reins were dropped and coming to a dead stop when reined in.

Today the reins are dangling to the ground. Inflation has disappeared and the federal-funds rate is negligible. Will the horse once again feel his oats?

Stay tuned. There are reasons to believe that this time is different because the bursting of the housing bubble has no analogy in earlier recessions. No one pulled back on the reins this time. Instead, the horse ran himself ragged. It will take a while for him to regain his strength.

© 2008 Michael B. Lehmann

The Lehmann Letter ©

Today the Federal Reserve reduced its federal-funds-rate target to between 0% and ¼%. You can read the Fed’s press release at:

http://www.federalreserve.gov/newsevents/press/monetary/20081216b.htm .

Direct your attention to these key passages:

“Since the Committee's last meeting, labor market conditions have deteriorated, and the available data indicate that consumer spending, business investment, and industrial production have declined. Financial markets remain quite strained and credit conditions tight. Overall, the outlook for economic activity has weakened further……

“The Federal Reserve will employ all available tools to promote the resumption of sustainable economic growth and to preserve price stability. In particular, the Committee anticipates that weak economic conditions are likely to warrant exceptionally low levels of the federal funds rate for some time…….. “

The patient is in intensive care and the Fed is administering its strongest medicine. Will it work?

We’ll see. The Fed’s efforts are certainly superior to maintaining high interest rates in the face of the economy’s collapse. But will rock-bottom interest rates actively promote recovery?

During the 2000-2002 dot-com bust the Fed also promoted interest-rates’ decline. Fortunately housing and autos responded favorably to these cuts, remained strong, and then blossomed by rising to sustained levels not seen before. Unfortunately we know how that story ended. Housing collapsed under its own bloated weight and dragged autos down with it. Falling interest rates have not yet resurrect these key sectors.

During earlier business cycles, in the 1960s and 1970s, a surging economy – booming housing and autos - ignited inflation and rising interest rates. Higher prices and higher borrowing costs choked-off the boom – slumping housing and autos - and led to recession. But these slumps were self-correcting because recession’s depressed conditions reduced inflation and interest rates, thereby reigniting – housing and autos - economic growth.

The economy behaved like a frisky horse in these earlier cycles, charging ahead when the reins were dropped and coming to a dead stop when reined in.

Today the reins are dangling to the ground. Inflation has disappeared and the federal-funds rate is negligible. Will the horse once again feel his oats?

Stay tuned. There are reasons to believe that this time is different because the bursting of the housing bubble has no analogy in earlier recessions. No one pulled back on the reins this time. Instead, the horse ran himself ragged. It will take a while for him to regain his strength.

© 2008 Michael B. Lehmann

Monday, December 15, 2008

Liquidity Trap

THE BE YOUR OWN ECONOMIST ® BLOG

The Lehmann Letter ©

In his 1936 “General Theory Of Employment, Interest and Money,” John Maynard Keynes discussed what he called the liquidity trap. The trap occurred when demand had pushed bond prices – think U.S. Treasury securities – so high that they could rise no further. At that point, in an economy awash in liquidity, interest rates hit rock bottom at barely above zero.

Keep in mind that bond prices and interest rates very inversely. Let’s say a 30-year bond sells for $1,000 and pays $50 annual interest for a 5% yield. If at any time in those 30 years the bond’s purchaser sells the bond, the change in the bond’s price will determine the rate of interest (yield) because the bond always pays $50 annually. For instance, if heavy demand for the bond pushed its price up to $2,000, then the yield would be roughly 2-1/2% ($50/$2,000 = 2-1/2%). If weak demand reduced the bond’s price to $500, then the yield would have risen to roughly 10% ($50/$500 = 10%).

In a weak economy, said Mr. Keynes, businesses had excess funds because of the dearth of projects in which to invest those funds. These circumstances prompted businesses to purchase bonds with their excess funds in order to earn a return on those funds. Unfortunately, excess liquidity could prompt massive demand for bonds, pushing their prices upward and their yield downward. Since the yield could not fall below zero, that set an upward boundary on bond prices.

When bond prices reached their maximum and bond yields dipped to their minimum, the economy was in the liquidity trap. The trap rendered monetary policy useless because the central bank could not further depress interest rates in order to implement an expansionary monetary policy. If business required lower rates before it purchased more plant and equipment, business would be disappointed. Rates could not fall and therefore business investment would not rise. The economy was stuck in the trap.

Our economy may be in, or close to, a liquidity trap today. Yields on some Treasury securities have briefly fallen to zero. The Federal Reserve is contemplating a drop in the federal-funds rate to less than 1%. Will this prompt business to invest more (purchase additional plant and equipment)? Probably not. Will households buy more homes and cars? That remains to be seen. The direction of home prices and employment will play an important role.

If the economy is caught in a liquidity trap, traditional monetary policy can have little effect.

© 2008 Michael B. Lehmann

The Lehmann Letter ©

In his 1936 “General Theory Of Employment, Interest and Money,” John Maynard Keynes discussed what he called the liquidity trap. The trap occurred when demand had pushed bond prices – think U.S. Treasury securities – so high that they could rise no further. At that point, in an economy awash in liquidity, interest rates hit rock bottom at barely above zero.

Keep in mind that bond prices and interest rates very inversely. Let’s say a 30-year bond sells for $1,000 and pays $50 annual interest for a 5% yield. If at any time in those 30 years the bond’s purchaser sells the bond, the change in the bond’s price will determine the rate of interest (yield) because the bond always pays $50 annually. For instance, if heavy demand for the bond pushed its price up to $2,000, then the yield would be roughly 2-1/2% ($50/$2,000 = 2-1/2%). If weak demand reduced the bond’s price to $500, then the yield would have risen to roughly 10% ($50/$500 = 10%).

In a weak economy, said Mr. Keynes, businesses had excess funds because of the dearth of projects in which to invest those funds. These circumstances prompted businesses to purchase bonds with their excess funds in order to earn a return on those funds. Unfortunately, excess liquidity could prompt massive demand for bonds, pushing their prices upward and their yield downward. Since the yield could not fall below zero, that set an upward boundary on bond prices.

When bond prices reached their maximum and bond yields dipped to their minimum, the economy was in the liquidity trap. The trap rendered monetary policy useless because the central bank could not further depress interest rates in order to implement an expansionary monetary policy. If business required lower rates before it purchased more plant and equipment, business would be disappointed. Rates could not fall and therefore business investment would not rise. The economy was stuck in the trap.

Our economy may be in, or close to, a liquidity trap today. Yields on some Treasury securities have briefly fallen to zero. The Federal Reserve is contemplating a drop in the federal-funds rate to less than 1%. Will this prompt business to invest more (purchase additional plant and equipment)? Probably not. Will households buy more homes and cars? That remains to be seen. The direction of home prices and employment will play an important role.

If the economy is caught in a liquidity trap, traditional monetary policy can have little effect.

© 2008 Michael B. Lehmann

Friday, December 12, 2008

Deflation’s Root

THE BE YOUR OWN ECONOMIST ® BLOG

The Lehmann Letter ©

Yesterday the Federal Reserve released its third-quarter 2008 flow-of-funds report. Households’ $117.4 billion reduction in outstanding debt caught the attention of many. Consumers are pulling back.

But there was another aspect of the report that generated less attention. To review the numbers for yourself, go to (http://www.federalreserve.gov/releases/z1/Current/z1r-2.pdf).

Calculate total private nonfinancial borrowing by subtracting federal borrowing from the total for all domestic nonfinancial sectors and then adding foreign borrowing. You should arrive at these totals for 2008.

2008

First Quarter $1,555.0 Billion

Second Quarter $772.0 Billion

Third Quarter -$277.7 Billion

The following chart is current through the second quarter. Update the chart in your mind’s eye by including the third quarter drop of -$277.7 billion.

Private Borrowing

(Click on chart to enlarge)

(The chart was taken from http://www.beyourowneconomist.com. [Click on Seminars and then Charts.] Go there for additional charts on the economy and a list of economic indicators.)

© 2008 Michael B. Lehmann

The Lehmann Letter ©

Yesterday the Federal Reserve released its third-quarter 2008 flow-of-funds report. Households’ $117.4 billion reduction in outstanding debt caught the attention of many. Consumers are pulling back.

But there was another aspect of the report that generated less attention. To review the numbers for yourself, go to (http://www.federalreserve.gov/releases/z1/Current/z1r-2.pdf).

Calculate total private nonfinancial borrowing by subtracting federal borrowing from the total for all domestic nonfinancial sectors and then adding foreign borrowing. You should arrive at these totals for 2008.

2008

First Quarter $1,555.0 Billion

Second Quarter $772.0 Billion

Third Quarter -$277.7 Billion

The following chart is current through the second quarter. Update the chart in your mind’s eye by including the third quarter drop of -$277.7 billion.

Private Borrowing

(Click on chart to enlarge)

(Recessions shaded)

This is the first time that private borrowing was negative. That is, the private sector is repaying its debts rather than incurring new debt. So what, you might say. Isn’t it about time the borrowing binge came to an end?

Not so fast. Borrowing supports spending. The surge in household and business indebtedness since 1990 financed the growth in aggregate demand. Mortgage borrowing’s support of residential construction is the most clear cut example, but not the only one. And borrowing’s current collapse is, of course, an obvious sign of the current recession’s seriousness.

Moreover, borrowing’s collapse is also an omen of impending deflation. It’s difficult to maintain prices when demand’s most important prop – borrowing – disappears.

This is the first time that private borrowing was negative. That is, the private sector is repaying its debts rather than incurring new debt. So what, you might say. Isn’t it about time the borrowing binge came to an end?

Not so fast. Borrowing supports spending. The surge in household and business indebtedness since 1990 financed the growth in aggregate demand. Mortgage borrowing’s support of residential construction is the most clear cut example, but not the only one. And borrowing’s current collapse is, of course, an obvious sign of the current recession’s seriousness.

Moreover, borrowing’s collapse is also an omen of impending deflation. It’s difficult to maintain prices when demand’s most important prop – borrowing – disappears.

(The chart was taken from http://www.beyourowneconomist.com. [Click on Seminars and then Charts.] Go there for additional charts on the economy and a list of economic indicators.)

© 2008 Michael B. Lehmann

Wednesday, December 10, 2008

Consumer Credit

THE BE YOUR OWN ECONOMIST ® BLOG

The Lehmann Letter ©

Today the nation closely followed news of the auto-industry rescue package.

Last Friday, December 5th, the Federal Reserve released its consumer-credit report (http://www.federalreserve.gov/releases/g19/Current/). These data have a direct bearing on the auto industry’s problems because consumers borrow heavily to finance motor-vehicle purchases.

You can see from the chart below that consumer credit has grown by about $100 billion a month for the last five years. But the most recent entry spiked downward. Was this an aberration?

Consumer Credit

(Click on chart to enlarge)

Recessions shaded

It’s too early to tell.

The Fed publishes historical data (http://www.federalreserve.gov/releases/g19/hist/cc_hist_sa.html ) that lets you calculate recent changes. Just subtract one month from the next and multiply by 12 to estimate an annual rate.

Here are the most recent figures.

July = +$88.0 billion

Aug = -$77.1 billion

Sep = +$80.8 billion

Oct = -$42.4 billion

You can see that September bounced back from August’s negative reading. Then October slipped below zero again. Over the last few months the reading’s average has been barely positive, not close to the $100 billion average of the last five years.

The credit crisis explains part of the decline. Borrowers have increasing difficulty qualifying for auto loans. But that’s not the whole story. Households are less likely to borrow and spend when they feel pessimistic. And recently consumer confidence has fallen dramatically. That may also be responsible for the recent slippage in these numbers.

Stay tuned to this statistic to see whether or not it continues to provide a signal of economic weakness.

(The chart was taken from http://www.beyourowneconomist.com. [Click on Seminars and then Charts.] Go there for additional charts on the economy and a list of economic indicators.)

© 2008 Michael B. Lehmann

The Lehmann Letter ©

Today the nation closely followed news of the auto-industry rescue package.

Last Friday, December 5th, the Federal Reserve released its consumer-credit report (http://www.federalreserve.gov/releases/g19/Current/). These data have a direct bearing on the auto industry’s problems because consumers borrow heavily to finance motor-vehicle purchases.

You can see from the chart below that consumer credit has grown by about $100 billion a month for the last five years. But the most recent entry spiked downward. Was this an aberration?

Consumer Credit

(Click on chart to enlarge)

Recessions shaded

It’s too early to tell.

The Fed publishes historical data (http://www.federalreserve.gov/releases/g19/hist/cc_hist_sa.html ) that lets you calculate recent changes. Just subtract one month from the next and multiply by 12 to estimate an annual rate.

Here are the most recent figures.

July = +$88.0 billion

Aug = -$77.1 billion

Sep = +$80.8 billion

Oct = -$42.4 billion

You can see that September bounced back from August’s negative reading. Then October slipped below zero again. Over the last few months the reading’s average has been barely positive, not close to the $100 billion average of the last five years.

The credit crisis explains part of the decline. Borrowers have increasing difficulty qualifying for auto loans. But that’s not the whole story. Households are less likely to borrow and spend when they feel pessimistic. And recently consumer confidence has fallen dramatically. That may also be responsible for the recent slippage in these numbers.

Stay tuned to this statistic to see whether or not it continues to provide a signal of economic weakness.

(The chart was taken from http://www.beyourowneconomist.com. [Click on Seminars and then Charts.] Go there for additional charts on the economy and a list of economic indicators.)

© 2008 Michael B. Lehmann

Monday, December 8, 2008

Obama Has It Right

THE BE YOUR OWN ECONOMIST ® BLOG

The Lehmann Letter ©

Today’s news reported that President-elect Obama favors a massive public-works program to boost aggregate demand and employment, a rescue for Detroit to avoid the risk of bankruptcy for the Big Three and expanded relief for homeowners facing foreclosure.

Right on!

The American people have to believe that our government is taking the lead in fighting recession, not sitting on the sidelines. That’s key to boosting confidence and private expenditures. Small measures won’t do. Relief must be stunning and occur forthwith. A trillion dollars is a good start. There’s much to be done. And why risk the damage of auto-company bankruptcies? Detroit can be assisted and restructured. It’s not one or the other. Finally, why should one more homeowner face immediate foreclosure? The new president should stop the foreclosures and institute an aggressive homeowner-rescue plan. Some homes will inevitably face foreclosure no matter what is done. But why let the value of out neighborhoods be dragged down any more than is absolutely necessary?

© 2008 Michael B. Lehmann

The Lehmann Letter ©

Today’s news reported that President-elect Obama favors a massive public-works program to boost aggregate demand and employment, a rescue for Detroit to avoid the risk of bankruptcy for the Big Three and expanded relief for homeowners facing foreclosure.

Right on!

The American people have to believe that our government is taking the lead in fighting recession, not sitting on the sidelines. That’s key to boosting confidence and private expenditures. Small measures won’t do. Relief must be stunning and occur forthwith. A trillion dollars is a good start. There’s much to be done. And why risk the damage of auto-company bankruptcies? Detroit can be assisted and restructured. It’s not one or the other. Finally, why should one more homeowner face immediate foreclosure? The new president should stop the foreclosures and institute an aggressive homeowner-rescue plan. Some homes will inevitably face foreclosure no matter what is done. But why let the value of out neighborhoods be dragged down any more than is absolutely necessary?

© 2008 Michael B. Lehmann

Friday, December 5, 2008

The Crisis Deepens

THE BE YOUR OWN ECONOMIST ® BLOG

The Lehmann Letter ©

This morning’s employment report from the Bureau of Labor Statistics is alarming (http://stats.bls.gov/news.release/empsit.nr0.htm):

“Nonfarm payroll employment fell sharply (-533,000) in November, and

the unemployment rate rose from 6.5 to 6.7 percent, the Bureau of Labor

Statistics of the U.S. Department of Labor reported today. November's

drop in payroll employment followed declines of 403,000 in September and

320,000 in October, as revised. Job losses were large and widespread

across the major industry sectors in November.”

November’s job loss – 533,000 – signals deep recession. So does the upward revision of the September and October figures to 403,000 and 320,000 respectively. Details of the report are equally grim. Only education and health services (+52,000) and government (+9,000) added jobs. All other sectors shed workers. The sharp drop in overall service employment (370,000) was especially eye-catching. This slump is not confined to construction and manufacturing.

When will the administration step in and stop the bleeding? A lower interest rate for home-buyers is good. A foreclosure moratorium for homeowners, together with a generous refinance package for those at risk of losing their homes, would be better. It’s hard to envision a successful recovery program that fails to include real-estate stabilization.

© 2008 Michael B. Lehmann

The Lehmann Letter ©

This morning’s employment report from the Bureau of Labor Statistics is alarming (http://stats.bls.gov/news.release/empsit.nr0.htm):

“Nonfarm payroll employment fell sharply (-533,000) in November, and

the unemployment rate rose from 6.5 to 6.7 percent, the Bureau of Labor

Statistics of the U.S. Department of Labor reported today. November's

drop in payroll employment followed declines of 403,000 in September and

320,000 in October, as revised. Job losses were large and widespread

across the major industry sectors in November.”

November’s job loss – 533,000 – signals deep recession. So does the upward revision of the September and October figures to 403,000 and 320,000 respectively. Details of the report are equally grim. Only education and health services (+52,000) and government (+9,000) added jobs. All other sectors shed workers. The sharp drop in overall service employment (370,000) was especially eye-catching. This slump is not confined to construction and manufacturing.

When will the administration step in and stop the bleeding? A lower interest rate for home-buyers is good. A foreclosure moratorium for homeowners, together with a generous refinance package for those at risk of losing their homes, would be better. It’s hard to envision a successful recovery program that fails to include real-estate stabilization.

© 2008 Michael B. Lehmann

Wednesday, December 3, 2008

December Publication Schedule & Web Sources

THE BE YOUR OWN ECONOMIST ® BLOG

The Lehmann Letter ©

You can use the WEB SOURCES listing (below) to find the data on your own and read the accompanying press release. The addresses take you to the source’s home page and the steps tell you how to navigate the site. That way (rather than provide a direct link to the data) you can become familiar with these sites and find additional information on your own.

PUBLICATION SCHEDULE

December 2008

Source (* below)…………Series Description…………Day & Date

Quarterly Data

BLS……………………….Productivity………………..….Wed, 3rd

BEA……………International transactions………….Wed, 17th

BEA…………………………GDP…………………….....……Tue, 23rd

Monthly Data

ISM………………….Purchasing managers’ index……….Mon, 1st

Fed…………………………..Consumer credit………..…….Fri, 5th

BLS………………………….Employment………………… Fri, 5th

Census……………………...Balance of trade………………Thu, 11th

BLS………………………….Producer prices……………….Fri, 12th

Census……………………...Retail trade…………………….Fri, 12th

Census……………………...Inventories……………………..Fri, 12th

Fed…………………………..Industrial production………….Mon, 15th

Fed………………………….Capacity utilization…………….Mon, 15th

BLS………………………….Consumer prices……………...Tue, 16th

Census……………………..Housing starts………………….Tue, 16th

Conf Bd…………………….Leading indicators…………….Thu, 18th

Census……………………..New-home sales……………….Tue, 23rd

NAR…………………………Existing-home sales…….…….Tue, 23rd

Census…………………….Capital goods……………….…..Wed, 24th

Conf Bd…………………….Consumer confidence…………Tue, 30th

* BEA = Bureau of Economic Analysis of the U.S. Department of Commerce

* BLS = Bureau of Labor Statistics of the U.S. Department of Labor

* Census = U.S. Bureau of the Census

* Conf Bd = Conference Board

* Fed = Federal Reserve System

* ISM = Institute for Supply Management

* NAR = National Association of Realtors

WEB SOURCES

Index of Leading Economic Indicators: http://www.conference-board.org/..........

Step 1: Click on "Economics" in the left-hand menu bar…………………………………….

Step 2: Click on "Economic Indicators" under "Economics" in the left-hand menu bar………………………………………………………………………………………………………………..

Step 3: Click on link under "U.S. Leading Indicators"………………………………………

Gross Domestic Product: http://www.bea.gov/....................................................

Step 1: Click on "Gross Domestic Product" under "National"………………………….

Step 2: Click on "National Income and Product Accounts Tables" under "Gross Domestic Product (GDP)"……………………………………………………………………………

Step 3: Click on "list of all NIPA Tables"………………………………………………………….

Step 4: Click on "Table 1.1.6. Real Gross Domestic Product..." and "Table 1.1.1. Percent Change..."……………………………………………………………………………………….

Step 5: Scroll down to line 1 in both tables and go to the last column on the right

Industrial Production & Capacity Utilization: http://www.federalreserve.gov/

Step 1: Click on "All Statistical Releases" under "Recent Statistical Releases" and then click on "Industrial Production and Capacity Utilization" under "Principal Economic Indicators" in the upper left…………………………………………………………

Step 2: Find the latest monthly data in the table next to "Total index" and "Total industry"……………………………………………………………………………………………………..

Institute For Supply Management Index: http://www.ism.ws/ ……………………….

Step 1: Click on "ISM Report on Business" in left-hand menu bar……………………

Step 2: Click on “Latest Manufacturing ROB” and find the latest PMI…………….

Producer Prices: http://stats.bls.gov/.....................................................................

Step 1: Click on “Producer Price Indexes” under “Inflation & Consumer Spending” in left-hand menu bar………………………………………………………………….

Step 2: Note "Finished goods" under "Latest Numbers" in upper right and multiply by 12 to put the data on an annual basis……………………………………….

Business Capital Expenditures (Nondefense Capital Goods): http://www.census.gov/ ………………………………………………………………………………..

Step 1: Click on "Economic Indicators" in the lower right…………………………………

Step 2: Click on "PDF" on the left under "Advance Report on Durable Goods Manufacturers' Shipments and Orders"…………………………………………………………..

Step 3: Scroll down to Table 1 and find new orders for nondefense capital goods near the bottom……………………………………………………………………………………………..

Inventories, Sales & Inventory/Sales Ratio: http://www.census.gov/

Step 1: Click on "Economic Indicators" in the lower right…………………………………

Step 2: Click on "HTML" on the left under "Manufacturing and Trade Inventories and Sales" ………………………………………………………………………………………………

Step 3: Scroll down to Table 1 and subtract previous month's inventories from latest month's and multiply by 12 to obtain inventory change, and then obtain the most recent inventory/sales ratio……………………………………………………………………

Consumer Price Index: http://stats.bls.gov/...........................................................

Step 1: Click on “Consumer Price Index” under “Inflation & Consumer Spending” in left-hand menu bar………………………………………………………………………………….

Step 2: Note "CPI-U..." at the top under "Latest Numbers" in upper right and multiply "SA" by 12 to put the data on an annual basis…………………………………..

Employment Data (Total Non-farm Payroll Employment) (Unemployment Rate) (Manufacturing Workweek): http://stats.bls.gov/ ………………………………………..

Step 1: Click on “National Employment” under “Employment & Unemployment” in right-hand menu bar………………………………………………………………………………

Step 2: Click on (HTML) following “Employment Situation Summary” under "Economic News Releases"……………………………………………………………………….

Step 3: Click on “Employment Situation Summary” under “Table of Contents”

Step 4: Scroll down to Table A and find the unemployment rate for all workers in the latest month, the change in nonfarm employment in the last column and manufacturing hours of work for the latest month…………………………………………..

Personal Income: http://www.bea.gov/.....................................................................

Step 1: Click on "Gross Domestic Product" under "National"……………………………..

Step 2: Click on "National Income and Product Accounts Tables" under "Gross Domestic Product (GDP)"…………………………………………………………………………….

Step 3: Click on "list of all NIPA Tables"……………………………………………………….

Step 4: Click on "Table 2.6 Personal Income..."…………………………………………………

Step 5: Scroll down to line 1…………………………………………………………………………..

Consumer Confidence: http://www.conference-board.org/....................................

Step 1: Click on the "Economics" in the left-hand menu bar……………………………….

Step 2: Click on "Economic Indicators" under "Economics" in the left-hand menu bar………………………………………………………………………………………………………………..

Step 3: Click on link under "Consumer Confidence Index"…………………………………

Consumer Credit: http://www.federalreserve.gov/...................................................

Step 1: Click on "All Statistical Releases" under "Recent Statistical Releases" and then click on "Consumer credit -- G19" under "Household Finance" in the upper right…………………………………………………………………………………………………………..

Step 2: Click on "Current Release"…………………………………………………………………

Step 3: Go to "Amount ... billions of dollars" and subtract previous month from current month & multiply by 12 to obtain seasonally adjusted dollar amount at annual rate………………………………………………………………………………………………..

Housing Starts: http://www.census.gov/..................................................................

Step 1: Click on "Economic Indicators" in the lower right………………………………….

Step 2: Click on "PDF" on the left under "Current Press Release" under "Housing Starts/Building Permits"………………………………………………………………………………..

Step 3: Scroll down to "Housing Starts"…………………………………………………………..

Home Sales (Existing-Home Sales): http://www.realtor.org/.................................

Step 1: Click on "Research" in the left-hand menu bar……………………………………….

Step 2: Find "Existing-Home Sales" under "Housing Indicators"……………………..

Home Sales (New-Home Sales): http://www.census.gov/.......................................

Step 1: Click on "Economic Indicators" in the lower right………………………………..

Step 2: Click on "PDF" on the left under "Current Press Release" under "New Home Sales"………………………………………………………………………………………………….

Retail Sales: http://www.census.gov/.......................................................................

Step 1: Click on "Economic Indicators" in the lower right…………………………………..

Step 2: Scroll down to "Advance Monthly Sales for Retail and Food Services" and click on "HTML" on the left under "Current Press Release"………………………………

© 2008 Michael B. Lehmann

The Lehmann Letter ©

You can use the WEB SOURCES listing (below) to find the data on your own and read the accompanying press release. The addresses take you to the source’s home page and the steps tell you how to navigate the site. That way (rather than provide a direct link to the data) you can become familiar with these sites and find additional information on your own.

PUBLICATION SCHEDULE

December 2008

Source (* below)…………Series Description…………Day & Date

Quarterly Data

BLS……………………….Productivity………………..….Wed, 3rd

BEA……………International transactions………….Wed, 17th

BEA…………………………GDP…………………….....……Tue, 23rd

Monthly Data

ISM………………….Purchasing managers’ index……….Mon, 1st

Fed…………………………..Consumer credit………..…….Fri, 5th

BLS………………………….Employment………………… Fri, 5th

Census……………………...Balance of trade………………Thu, 11th

BLS………………………….Producer prices……………….Fri, 12th

Census……………………...Retail trade…………………….Fri, 12th

Census……………………...Inventories……………………..Fri, 12th

Fed…………………………..Industrial production………….Mon, 15th

Fed………………………….Capacity utilization…………….Mon, 15th

BLS………………………….Consumer prices……………...Tue, 16th

Census……………………..Housing starts………………….Tue, 16th

Conf Bd…………………….Leading indicators…………….Thu, 18th

Census……………………..New-home sales……………….Tue, 23rd

NAR…………………………Existing-home sales…….…….Tue, 23rd

Census…………………….Capital goods……………….…..Wed, 24th

Conf Bd…………………….Consumer confidence…………Tue, 30th

* BEA = Bureau of Economic Analysis of the U.S. Department of Commerce

* BLS = Bureau of Labor Statistics of the U.S. Department of Labor

* Census = U.S. Bureau of the Census

* Conf Bd = Conference Board

* Fed = Federal Reserve System

* ISM = Institute for Supply Management

* NAR = National Association of Realtors

WEB SOURCES

Index of Leading Economic Indicators: http://www.conference-board.org/..........

Step 1: Click on "Economics" in the left-hand menu bar…………………………………….

Step 2: Click on "Economic Indicators" under "Economics" in the left-hand menu bar………………………………………………………………………………………………………………..

Step 3: Click on link under "U.S. Leading Indicators"………………………………………

Gross Domestic Product: http://www.bea.gov/....................................................

Step 1: Click on "Gross Domestic Product" under "National"………………………….

Step 2: Click on "National Income and Product Accounts Tables" under "Gross Domestic Product (GDP)"……………………………………………………………………………

Step 3: Click on "list of all NIPA Tables"………………………………………………………….

Step 4: Click on "Table 1.1.6. Real Gross Domestic Product..." and "Table 1.1.1. Percent Change..."……………………………………………………………………………………….

Step 5: Scroll down to line 1 in both tables and go to the last column on the right

Industrial Production & Capacity Utilization: http://www.federalreserve.gov/

Step 1: Click on "All Statistical Releases" under "Recent Statistical Releases" and then click on "Industrial Production and Capacity Utilization" under "Principal Economic Indicators" in the upper left…………………………………………………………

Step 2: Find the latest monthly data in the table next to "Total index" and "Total industry"……………………………………………………………………………………………………..

Institute For Supply Management Index: http://www.ism.ws/ ……………………….

Step 1: Click on "ISM Report on Business" in left-hand menu bar……………………

Step 2: Click on “Latest Manufacturing ROB” and find the latest PMI…………….

Producer Prices: http://stats.bls.gov/.....................................................................

Step 1: Click on “Producer Price Indexes” under “Inflation & Consumer Spending” in left-hand menu bar………………………………………………………………….

Step 2: Note "Finished goods" under "Latest Numbers" in upper right and multiply by 12 to put the data on an annual basis……………………………………….

Business Capital Expenditures (Nondefense Capital Goods): http://www.census.gov/ ………………………………………………………………………………..

Step 1: Click on "Economic Indicators" in the lower right…………………………………

Step 2: Click on "PDF" on the left under "Advance Report on Durable Goods Manufacturers' Shipments and Orders"…………………………………………………………..

Step 3: Scroll down to Table 1 and find new orders for nondefense capital goods near the bottom……………………………………………………………………………………………..

Inventories, Sales & Inventory/Sales Ratio: http://www.census.gov/

Step 1: Click on "Economic Indicators" in the lower right…………………………………

Step 2: Click on "HTML" on the left under "Manufacturing and Trade Inventories and Sales" ………………………………………………………………………………………………

Step 3: Scroll down to Table 1 and subtract previous month's inventories from latest month's and multiply by 12 to obtain inventory change, and then obtain the most recent inventory/sales ratio……………………………………………………………………

Consumer Price Index: http://stats.bls.gov/...........................................................

Step 1: Click on “Consumer Price Index” under “Inflation & Consumer Spending” in left-hand menu bar………………………………………………………………………………….

Step 2: Note "CPI-U..." at the top under "Latest Numbers" in upper right and multiply "SA" by 12 to put the data on an annual basis…………………………………..

Employment Data (Total Non-farm Payroll Employment) (Unemployment Rate) (Manufacturing Workweek): http://stats.bls.gov/ ………………………………………..

Step 1: Click on “National Employment” under “Employment & Unemployment” in right-hand menu bar………………………………………………………………………………

Step 2: Click on (HTML) following “Employment Situation Summary” under "Economic News Releases"……………………………………………………………………….

Step 3: Click on “Employment Situation Summary” under “Table of Contents”

Step 4: Scroll down to Table A and find the unemployment rate for all workers in the latest month, the change in nonfarm employment in the last column and manufacturing hours of work for the latest month…………………………………………..

Personal Income: http://www.bea.gov/.....................................................................

Step 1: Click on "Gross Domestic Product" under "National"……………………………..

Step 2: Click on "National Income and Product Accounts Tables" under "Gross Domestic Product (GDP)"…………………………………………………………………………….

Step 3: Click on "list of all NIPA Tables"……………………………………………………….

Step 4: Click on "Table 2.6 Personal Income..."…………………………………………………

Step 5: Scroll down to line 1…………………………………………………………………………..

Consumer Confidence: http://www.conference-board.org/....................................

Step 1: Click on the "Economics" in the left-hand menu bar……………………………….

Step 2: Click on "Economic Indicators" under "Economics" in the left-hand menu bar………………………………………………………………………………………………………………..

Step 3: Click on link under "Consumer Confidence Index"…………………………………

Consumer Credit: http://www.federalreserve.gov/...................................................

Step 1: Click on "All Statistical Releases" under "Recent Statistical Releases" and then click on "Consumer credit -- G19" under "Household Finance" in the upper right…………………………………………………………………………………………………………..

Step 2: Click on "Current Release"…………………………………………………………………

Step 3: Go to "Amount ... billions of dollars" and subtract previous month from current month & multiply by 12 to obtain seasonally adjusted dollar amount at annual rate………………………………………………………………………………………………..

Housing Starts: http://www.census.gov/..................................................................

Step 1: Click on "Economic Indicators" in the lower right………………………………….

Step 2: Click on "PDF" on the left under "Current Press Release" under "Housing Starts/Building Permits"………………………………………………………………………………..

Step 3: Scroll down to "Housing Starts"…………………………………………………………..

Home Sales (Existing-Home Sales): http://www.realtor.org/.................................

Step 1: Click on "Research" in the left-hand menu bar……………………………………….

Step 2: Find "Existing-Home Sales" under "Housing Indicators"……………………..

Home Sales (New-Home Sales): http://www.census.gov/.......................................

Step 1: Click on "Economic Indicators" in the lower right………………………………..

Step 2: Click on "PDF" on the left under "Current Press Release" under "New Home Sales"………………………………………………………………………………………………….

Retail Sales: http://www.census.gov/.......................................................................

Step 1: Click on "Economic Indicators" in the lower right…………………………………..

Step 2: Scroll down to "Advance Monthly Sales for Retail and Food Services" and click on "HTML" on the left under "Current Press Release"………………………………

© 2008 Michael B. Lehmann

Tuesday, December 2, 2008

Autos and Manufacturing

THE BE YOUR OWN ECONOMIST ® BLOG

The Lehmann Letter ©

The Big Three are testifying before Congress again, trying to make their case for a bailout. Maybe they’ll succeed.

But there is something everyone can agree on: The automobile industry and all manufacturing are in trouble.

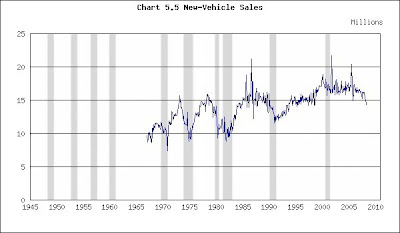

November new-vehicle sales were 10.1 million at a seasonally-adjusted annual rate. See where that is on the chart below. Is there any wonder that the industry is in crisis?

New-Vehicle Sales

(Click on chart to enlarge)

Recessions shaded

Yesterday the Institute for Supply Management said the Purchasing Managers’ Index fell to 36.2 in November (http://www.ism.ws/ ). In the chart below you need to go back to 1980 for a lower reading. The auto industry is a reflection of what is happening throughout manufacturing. Or vice versa.

Purchasing Managers’ Index

(Click on chart to enlarge)

Recessions shaded

In a couple of weeks the Fed will release its industrial production and capacity-utilization data. We’ll see if they, too, confirm these grim trends.

(The charts are taken from http://www.beyourowneconomist.com. [Click on Seminars and then Charts.] Go there for additional charts on the economy and a list of economic indicators.)

© 2008 Michael B. Lehmann

The Lehmann Letter ©

The Big Three are testifying before Congress again, trying to make their case for a bailout. Maybe they’ll succeed.

But there is something everyone can agree on: The automobile industry and all manufacturing are in trouble.

November new-vehicle sales were 10.1 million at a seasonally-adjusted annual rate. See where that is on the chart below. Is there any wonder that the industry is in crisis?

New-Vehicle Sales

(Click on chart to enlarge)

Recessions shaded

Yesterday the Institute for Supply Management said the Purchasing Managers’ Index fell to 36.2 in November (http://www.ism.ws/ ). In the chart below you need to go back to 1980 for a lower reading. The auto industry is a reflection of what is happening throughout manufacturing. Or vice versa.

Purchasing Managers’ Index

(Click on chart to enlarge)

Recessions shaded

In a couple of weeks the Fed will release its industrial production and capacity-utilization data. We’ll see if they, too, confirm these grim trends.

(The charts are taken from http://www.beyourowneconomist.com. [Click on Seminars and then Charts.] Go there for additional charts on the economy and a list of economic indicators.)

© 2008 Michael B. Lehmann

Monday, December 1, 2008

It’s Official

THE BE YOUR OWN ECONOMIST ® BLOG

The Lehmann Letter ©

Today the National Bureau of Economic Research announced (http://wwwdev.nber.org/cycles/dec2008.html) that “…a peak in economic activity occurred in the U.S. economy in December 2007. The peak marks the end of the expansion that began in November 2001 and the beginning of a recession. The expansion lasted 73 months; the previous expansion of the 1990s lasted 120 months.”

So there you have it. It’s official. We’re in a recession and have been for a year, despite the Bush administration’s reluctance to pin a tail on that donkey.

The Bureau justified its position by defining recession and employment’s key role in determining whether or not the economy is in recession:

“A recession is a significant decline in economic activity spread across the economy, lasting more than a few months, normally visible in production, employment, real income, and other indicators. A recession begins when the economy reaches a peak of activity and ends when the economy reaches its trough. Between trough and peak, the economy is in an expansion.

“Because a recession is a broad contraction of the economy, not confined to one sector, the committee emphasizes economy-wide measures of economic activity. The committee believes that domestic production and employment are the primary conceptual measures of economic activity.

“The committee views the payroll employment measure, which is based on a large survey of employers, as the most reliable comprehensive estimate of employment. This series reached a peak in December 2007 and has declined every month since then.”

“The Bureau believes that the decline in employment is the best evidence of recession.”

How long will the recession last?

Let’s ask Federal Reserve chairman Ben Bernanke. In a speech delivered today (http://www.federalreserve.gov/newsevents/speech/bernanke20081201a.htm) he said, “…the U.S. economy remains under considerable stress. …economic activity appears to have downshifted further in the wake of the deterioration in financial conditions in September…economic conditions will probably remain weak for a time. In particular, household spending likely will continue to be depressed by the declines to date in household wealth, cumulating job losses, weak consumer confidence, and a lack of credit availability.

“The global economy has also slowed. Many industrial countries were affected by the financial crisis from the beginning, but the latest economic data point to a more noticeable weakening of conditions. And emerging market economies, which were little affected at first, are slowing now as well. One implication of these developments is that exports are not likely to be as great a source of strength for U.S. economic activity in coming quarters as they had been earlier this year."

This recession will be a long one. It’s already a year old and there’s no end in sight. Quite to the contrary, it appears that conditions will deteriorate further before they improve.

Will this recession be the worst recession since the Great Depression of the 1930s? For that to occur, using unemployment as the single gauge, the unemployment rate would have to exceed (slightly more than) 10%, the level it reached during the 1981-82 recession. In October the unemployment rate was 6.5%. We have a ways to go. Let’s hope we don’t arrive.

© 2008 Michael B. Lehmann

The Lehmann Letter ©

Today the National Bureau of Economic Research announced (http://wwwdev.nber.org/cycles/dec2008.html) that “…a peak in economic activity occurred in the U.S. economy in December 2007. The peak marks the end of the expansion that began in November 2001 and the beginning of a recession. The expansion lasted 73 months; the previous expansion of the 1990s lasted 120 months.”

So there you have it. It’s official. We’re in a recession and have been for a year, despite the Bush administration’s reluctance to pin a tail on that donkey.

The Bureau justified its position by defining recession and employment’s key role in determining whether or not the economy is in recession:

“A recession is a significant decline in economic activity spread across the economy, lasting more than a few months, normally visible in production, employment, real income, and other indicators. A recession begins when the economy reaches a peak of activity and ends when the economy reaches its trough. Between trough and peak, the economy is in an expansion.

“Because a recession is a broad contraction of the economy, not confined to one sector, the committee emphasizes economy-wide measures of economic activity. The committee believes that domestic production and employment are the primary conceptual measures of economic activity.

“The committee views the payroll employment measure, which is based on a large survey of employers, as the most reliable comprehensive estimate of employment. This series reached a peak in December 2007 and has declined every month since then.”

“The Bureau believes that the decline in employment is the best evidence of recession.”

How long will the recession last?

Let’s ask Federal Reserve chairman Ben Bernanke. In a speech delivered today (http://www.federalreserve.gov/newsevents/speech/bernanke20081201a.htm) he said, “…the U.S. economy remains under considerable stress. …economic activity appears to have downshifted further in the wake of the deterioration in financial conditions in September…economic conditions will probably remain weak for a time. In particular, household spending likely will continue to be depressed by the declines to date in household wealth, cumulating job losses, weak consumer confidence, and a lack of credit availability.

“The global economy has also slowed. Many industrial countries were affected by the financial crisis from the beginning, but the latest economic data point to a more noticeable weakening of conditions. And emerging market economies, which were little affected at first, are slowing now as well. One implication of these developments is that exports are not likely to be as great a source of strength for U.S. economic activity in coming quarters as they had been earlier this year."

This recession will be a long one. It’s already a year old and there’s no end in sight. Quite to the contrary, it appears that conditions will deteriorate further before they improve.

Will this recession be the worst recession since the Great Depression of the 1930s? For that to occur, using unemployment as the single gauge, the unemployment rate would have to exceed (slightly more than) 10%, the level it reached during the 1981-82 recession. In October the unemployment rate was 6.5%. We have a ways to go. Let’s hope we don’t arrive.

© 2008 Michael B. Lehmann

Wednesday, November 26, 2008

Swimming Upstream

THE BE YOUR OWN ECONOMIST ® BLOG

The Lehmann Letter ©

President-elect Obama is doing all he can to build confidence that his administration will hit the deck running on January 20, 2009. His economic team is in place and he has made clear that stimulating economic recovery, not deficit reduction or balancing the budget, is his first priority.

Good for him. Everyone wishes him well.

But the statistical news remains grim. Yesterday the Bureau of Economic Analysis (BEA) confirmed that GDP fell in the third quarter. The announcement also said (http://www.bea.gov/newsreleases/national/gdp/gdpnewsrelease.htm): “Profits from current production (corporate profits with inventory valuation and capital consumption adjustments) decreased $14.6 billion in the third quarter, compared with a decrease of$60.2 billion in the second quarter.” As a matter of fact, corporate profits were lower than at any time since the fourth quarter of 2005, almost three years ago.

The BEA also reported that consumption expenditures dropped by one percent in October (http://www.bea.gov/newsreleases/national/pi/pinewsrelease.htm): “Personal income increased $42.4 billion, or 0.3 percent, and disposable personal income (DPI) increased $45.1 billion, or 0.4 percent, in October, according to the Bureau of Economic Analysis. Personal consumption expenditures (PCE) decreased $102.8 billion, or 1.0 percent.” Despite income growth, consumers reduced spending. That’s a clear sign of the fear and uncertainty that grips households. They’d rather build their balance sheets than spend their income.

Today the Census Bureau released new-home sales data for October (http://www.census.gov/const/newressales.pdf): “Sales of new one-family houses in October 2008 were at a seasonally adjusted annual rate of 433,000, according to estimates released jointly today by the U.S. Census Bureau and the Department of Housing and Urban Development. This is 5.3 percent (±15.0%)* below the revised September of 457,000 and is 40.1 percent (±9.9%) below the October 2007 estimate of 723,000.”

Home sales are 40% below last year’s level and about a low as they were in the 1900-91 recession. Almost 20 years of gains are gone.

The Census Bureau also reported (http://www.census.gov/indicator/www/m3/adv/pdf/durgd.pdf): “New orders for manufactured durable goods in October decreased $12.7 billion or 6.2 percent to $193.0 billion, the U.S. Census Bureau announced today. This was the largest percent decrease in new orders since October 2006 and followed two consecutive monthly decreases including a 0.2 percent September decrease…..Nondefense new orders for capital goods in October

decreased $2.4 billion or 3.6 percent to $65.6 billion.”

Durable-good manufacturing has stalled, especially new orders for nondefense capital goods. This is a leading indicator of business capital expenditures.

There you have it: Profits, consumer spending and business capital expenditures are all down sharply. The new president is doing what he can to instill confidence in the forthcoming administration, but he’s clearly swimming upstream.

© 2008 Michael B. Lehmann

The Lehmann Letter ©

President-elect Obama is doing all he can to build confidence that his administration will hit the deck running on January 20, 2009. His economic team is in place and he has made clear that stimulating economic recovery, not deficit reduction or balancing the budget, is his first priority.

Good for him. Everyone wishes him well.

But the statistical news remains grim. Yesterday the Bureau of Economic Analysis (BEA) confirmed that GDP fell in the third quarter. The announcement also said (http://www.bea.gov/newsreleases/national/gdp/gdpnewsrelease.htm): “Profits from current production (corporate profits with inventory valuation and capital consumption adjustments) decreased $14.6 billion in the third quarter, compared with a decrease of$60.2 billion in the second quarter.” As a matter of fact, corporate profits were lower than at any time since the fourth quarter of 2005, almost three years ago.

The BEA also reported that consumption expenditures dropped by one percent in October (http://www.bea.gov/newsreleases/national/pi/pinewsrelease.htm): “Personal income increased $42.4 billion, or 0.3 percent, and disposable personal income (DPI) increased $45.1 billion, or 0.4 percent, in October, according to the Bureau of Economic Analysis. Personal consumption expenditures (PCE) decreased $102.8 billion, or 1.0 percent.” Despite income growth, consumers reduced spending. That’s a clear sign of the fear and uncertainty that grips households. They’d rather build their balance sheets than spend their income.

Today the Census Bureau released new-home sales data for October (http://www.census.gov/const/newressales.pdf): “Sales of new one-family houses in October 2008 were at a seasonally adjusted annual rate of 433,000, according to estimates released jointly today by the U.S. Census Bureau and the Department of Housing and Urban Development. This is 5.3 percent (±15.0%)* below the revised September of 457,000 and is 40.1 percent (±9.9%) below the October 2007 estimate of 723,000.”

Home sales are 40% below last year’s level and about a low as they were in the 1900-91 recession. Almost 20 years of gains are gone.

The Census Bureau also reported (http://www.census.gov/indicator/www/m3/adv/pdf/durgd.pdf): “New orders for manufactured durable goods in October decreased $12.7 billion or 6.2 percent to $193.0 billion, the U.S. Census Bureau announced today. This was the largest percent decrease in new orders since October 2006 and followed two consecutive monthly decreases including a 0.2 percent September decrease…..Nondefense new orders for capital goods in October

decreased $2.4 billion or 3.6 percent to $65.6 billion.”

Durable-good manufacturing has stalled, especially new orders for nondefense capital goods. This is a leading indicator of business capital expenditures.

There you have it: Profits, consumer spending and business capital expenditures are all down sharply. The new president is doing what he can to instill confidence in the forthcoming administration, but he’s clearly swimming upstream.

© 2008 Michael B. Lehmann

Tuesday, November 25, 2008

A Step In The Right Direction

THE BE YOUR OWN ECONOMIST ® BLOG

The Lehmann Letter ©

Today the Fed announced two initiatives designed to hasten our emergence from the financial crisis (http://www.federalreserve.gov/newsevents/press/monetary/20081125a.htm and http://www.federalreserve.gov/newsevents/press/monetary/20081125b.htm.)

In the Fed’s own words:

“…the Term Asset-Backed Securities Loan Facility (TALF), (is) a facility that will help market participants meet the credit needs of households and small businesses by supporting the issuance of asset-backed securities (ABS) collateralized by student loans, auto loans, credit card loans, and loans guaranteed by the Small Business Administration (SBA).

“Under the TALF, the Federal Reserve Bank of New York (FRBNY) will lend up to $200 billion on a non-recourse basis to holders of certain AAA-rated ABS backed by newly and recently originated consumer and small business loans. The FRBNY will lend an amount equal to the market value of the ABS less a haircut and will be secured at all times by the ABS. The U.S. Treasury Department--under the Troubled Assets Relief Program (TARP) of the Emergency Economic Stabilization Act of 2008--will provide $20 billion of credit protection to the FRBNY in connection with the TALF….”

“New issuance of ABS declined precipitously in September and came to a halt in October. At the same time, interest rate spreads on AAA-rated tranches of ABS soared to levels well outside the range of historical experience, reflecting unusually high risk premiums. The ABS markets historically have funded a substantial share of consumer credit and SBA-guaranteed small business loans. Continued disruption of these markets could significantly limit the availability of credit to households and small businesses and thereby contribute to further weakening of U.S. economic activity. The TALF is designed to increase credit availability and support economic activity by facilitating renewed issuance of consumer and small business ABS at more normal interest rate spreads.”

In addition:

“The Federal Reserve … will initiate a program to purchase the direct obligations of housing-related government-sponsored enterprises (GSEs)--Fannie Mae, Freddie Mac, and the Federal Home Loan Banks--and mortgage-backed securities (MBS) backed by Fannie Mae, Freddie Mac, and Ginnie Mae. Spreads of rates on GSE debt and on GSE-guaranteed mortgages have widened appreciably of late. This action is being taken to reduce the cost and increase the availability of credit for the purchase of houses, which in turn should support housing markets and foster improved conditions in financial markets more generally…..”

The Fed, with the Treasury’s assistance, wants to boost household purchases of durable goods (by freeing consumer credit) and new homes (by freeing mortgage borrowing). These measures should help.

But note the dire conditions in the asset-backed and mortgage-backed securities markets as revealed by the following excerpts from the Fed’s press release:

“New issuance of ABS declined precipitously in September and came to a halt in October. At the same time, interest rate spreads on AAA-rated tranches of ABS soared to levels well outside the range of historical experience, reflecting unusually high risk premiums. ……….Spreads of rates on GSE debt and on GSE-guaranteed mortgages have widened appreciably of late.“

Will the Fed’s actions be sufficient? To what extent are households reducing their purchases of durable goods and homes because they can’t obtain credit and to what extent are households reducing their purchases because they want to protect their balance sheets? And what role does the ongoing collapse of home prices contribute to the crisis and households’ desire to protect their balance sheets?

Perhaps a general moratorium on home foreclosures and massive assistance to indebted homeowners, by attacking the root cause of the crisis (collapsing home values), is the requisite first step that must be taken before other measures can become fully effective.

© 2008 Michael B. Lehmann

The Lehmann Letter ©

Today the Fed announced two initiatives designed to hasten our emergence from the financial crisis (http://www.federalreserve.gov/newsevents/press/monetary/20081125a.htm and http://www.federalreserve.gov/newsevents/press/monetary/20081125b.htm.)

In the Fed’s own words:

“…the Term Asset-Backed Securities Loan Facility (TALF), (is) a facility that will help market participants meet the credit needs of households and small businesses by supporting the issuance of asset-backed securities (ABS) collateralized by student loans, auto loans, credit card loans, and loans guaranteed by the Small Business Administration (SBA).

“Under the TALF, the Federal Reserve Bank of New York (FRBNY) will lend up to $200 billion on a non-recourse basis to holders of certain AAA-rated ABS backed by newly and recently originated consumer and small business loans. The FRBNY will lend an amount equal to the market value of the ABS less a haircut and will be secured at all times by the ABS. The U.S. Treasury Department--under the Troubled Assets Relief Program (TARP) of the Emergency Economic Stabilization Act of 2008--will provide $20 billion of credit protection to the FRBNY in connection with the TALF….”

“New issuance of ABS declined precipitously in September and came to a halt in October. At the same time, interest rate spreads on AAA-rated tranches of ABS soared to levels well outside the range of historical experience, reflecting unusually high risk premiums. The ABS markets historically have funded a substantial share of consumer credit and SBA-guaranteed small business loans. Continued disruption of these markets could significantly limit the availability of credit to households and small businesses and thereby contribute to further weakening of U.S. economic activity. The TALF is designed to increase credit availability and support economic activity by facilitating renewed issuance of consumer and small business ABS at more normal interest rate spreads.”

In addition:

“The Federal Reserve … will initiate a program to purchase the direct obligations of housing-related government-sponsored enterprises (GSEs)--Fannie Mae, Freddie Mac, and the Federal Home Loan Banks--and mortgage-backed securities (MBS) backed by Fannie Mae, Freddie Mac, and Ginnie Mae. Spreads of rates on GSE debt and on GSE-guaranteed mortgages have widened appreciably of late. This action is being taken to reduce the cost and increase the availability of credit for the purchase of houses, which in turn should support housing markets and foster improved conditions in financial markets more generally…..”

The Fed, with the Treasury’s assistance, wants to boost household purchases of durable goods (by freeing consumer credit) and new homes (by freeing mortgage borrowing). These measures should help.

But note the dire conditions in the asset-backed and mortgage-backed securities markets as revealed by the following excerpts from the Fed’s press release:

“New issuance of ABS declined precipitously in September and came to a halt in October. At the same time, interest rate spreads on AAA-rated tranches of ABS soared to levels well outside the range of historical experience, reflecting unusually high risk premiums. ……….Spreads of rates on GSE debt and on GSE-guaranteed mortgages have widened appreciably of late.“

Will the Fed’s actions be sufficient? To what extent are households reducing their purchases of durable goods and homes because they can’t obtain credit and to what extent are households reducing their purchases because they want to protect their balance sheets? And what role does the ongoing collapse of home prices contribute to the crisis and households’ desire to protect their balance sheets?

Perhaps a general moratorium on home foreclosures and massive assistance to indebted homeowners, by attacking the root cause of the crisis (collapsing home values), is the requisite first step that must be taken before other measures can become fully effective.

© 2008 Michael B. Lehmann

Monday, November 24, 2008

The New President’s Dilemma

THE BE YOUR OWN ECONOMIST ® BLOG

The Lehmann Letter ©

The Following Op-Ed ran in The San Francisco Chronicle on November 12 (http://www.sfgate.com/cgi-bin/article.cgi?f=/c/a/2008/11/12/EDLJ142NQS.DTL&hw=Michael+Lehmann&sn=001&sc=1000) . It’s still true.

President-elect Barack Obama faces a dilemma.

A severe recession is unfolding. Demand, production, employment, income - all are falling and falling hard. The new president has two traditional remedies at his disposal: Reduce taxes so that consumers can purchase more, thereby stimulating production and employment, or increase public-works spending to directly boost employment. These remedies will, of course, raise the federal deficit.

Therein lies the dilemma: The president cannot effectively deal with the recession and shrink the deficit. Which horn of the dilemma should the president choose?

In the spring of 1933, the same dilemma confronted President Franklin D. Roosevelt. FDR had campaigned on a balanced-budget platform. But when he took office, events left him no choice. FDR'S administration enacted sweeping measures that lifted federal spending and the federal deficit. The Works Progress Administration and the Civilian Conservation Corps spent billions on public works and employed millions. The deficit grew.

Obama now confronts the most serious economic crisis and dilemma since the Great Depression. Like FDR, he must choose between promoting economic recovery and containing the deficit. He can't do both.

The new president can use the $700 billion bank bailout as a template. In that instance, Congress moved decisively to meet the financial crisis. President Obama should present Congress with an equally large, bold and urgent program of tax cuts and spending increases to deal immediately with the recession. Households living from hand to mouth will spend any increase in after-tax income or extension of unemployment benefits. Now is the time to invest in the nation's crumbling infrastructure and the energy-independence and green-technology programs that Obama advocated.

The deficit will grow dramatically and the new administration should deal with it as soon as economic recovery is assured. Meanwhile, interest rates have fallen and the dollar has strengthened, proving that foreign investors remain willing to invest in America. If the rest of the world wants to invest in America, why shouldn't we? Recession confronts us immediately; national bankruptcy does not.

Now is not the time to think small.

© 2008 Michael B. Lehmann

The Lehmann Letter ©

The Following Op-Ed ran in The San Francisco Chronicle on November 12 (http://www.sfgate.com/cgi-bin/article.cgi?f=/c/a/2008/11/12/EDLJ142NQS.DTL&hw=Michael+Lehmann&sn=001&sc=1000) . It’s still true.

President-elect Barack Obama faces a dilemma.

A severe recession is unfolding. Demand, production, employment, income - all are falling and falling hard. The new president has two traditional remedies at his disposal: Reduce taxes so that consumers can purchase more, thereby stimulating production and employment, or increase public-works spending to directly boost employment. These remedies will, of course, raise the federal deficit.

Therein lies the dilemma: The president cannot effectively deal with the recession and shrink the deficit. Which horn of the dilemma should the president choose?

In the spring of 1933, the same dilemma confronted President Franklin D. Roosevelt. FDR had campaigned on a balanced-budget platform. But when he took office, events left him no choice. FDR'S administration enacted sweeping measures that lifted federal spending and the federal deficit. The Works Progress Administration and the Civilian Conservation Corps spent billions on public works and employed millions. The deficit grew.

Obama now confronts the most serious economic crisis and dilemma since the Great Depression. Like FDR, he must choose between promoting economic recovery and containing the deficit. He can't do both.

The new president can use the $700 billion bank bailout as a template. In that instance, Congress moved decisively to meet the financial crisis. President Obama should present Congress with an equally large, bold and urgent program of tax cuts and spending increases to deal immediately with the recession. Households living from hand to mouth will spend any increase in after-tax income or extension of unemployment benefits. Now is the time to invest in the nation's crumbling infrastructure and the energy-independence and green-technology programs that Obama advocated.

The deficit will grow dramatically and the new administration should deal with it as soon as economic recovery is assured. Meanwhile, interest rates have fallen and the dollar has strengthened, proving that foreign investors remain willing to invest in America. If the rest of the world wants to invest in America, why shouldn't we? Recession confronts us immediately; national bankruptcy does not.

Now is not the time to think small.

© 2008 Michael B. Lehmann

Tuesday, November 11, 2008

Taking A Break

THE BE YOUR OWN ECONOMIST ® BLOG

The Lehmann Letter ©

The blogger will take a brief respite and return on or about November 19.

© 2008 Michael B. Lehmann

The Lehmann Letter ©

The blogger will take a brief respite and return on or about November 19.

© 2008 Michael B. Lehmann

What About Homeowners?

THE BE YOUR OWN ECONOMIST ® BLOG

The Lehmann Letter ©

Every day we learn the government bailout has been extended to more businesses or there’s an effort under way to broaden the bailout’s coverage.

The banks are gobbling up their share of the $700 billion package. AIG’s assistance has topped $100 billion. The automakers will probably receive a rescue package. American Express has obtained permission to become a bank in order to ease the strains facing its credit-card business.

Meanwhile, home prices continue to plunge as foreclosures grow. Millions will lose their homes and millions more will end up under water (mortgage debt exceeds home’s value). What’s fair about that? Why should homeowners suffer while financial institutions and manufacturers are thrown a life line?

Everyone knows what needs to be done. There should be an immediate 90-day moratorium on foreclosures. During that period mortgages should be written down to the property’s market value for those homeowners who can’t make their payments. This entails a means test, so one should be created. If the homeowner still can’t pay the mortgage, then the term of the loan should be extended and the interest rate reduced. The federal government can compensate the lender for any loss.

That would direct relief to those who need it most.

Would there be complaints by those not facing foreclosure because the means test demonstrated their ability to pay? Would they be jealous of those who received assistance when they did not? Perhaps. But it would still be worth it to stop the losses and halt the foreclosures.

Would prices stop falling? Probably not. But they would not fall as far as they will fall if we don’t stop the foreclosures.

Washington should stop thinking small!

© 2008 Michael B. Lehmann

The Lehmann Letter ©

Every day we learn the government bailout has been extended to more businesses or there’s an effort under way to broaden the bailout’s coverage.

The banks are gobbling up their share of the $700 billion package. AIG’s assistance has topped $100 billion. The automakers will probably receive a rescue package. American Express has obtained permission to become a bank in order to ease the strains facing its credit-card business.

Meanwhile, home prices continue to plunge as foreclosures grow. Millions will lose their homes and millions more will end up under water (mortgage debt exceeds home’s value). What’s fair about that? Why should homeowners suffer while financial institutions and manufacturers are thrown a life line?

Everyone knows what needs to be done. There should be an immediate 90-day moratorium on foreclosures. During that period mortgages should be written down to the property’s market value for those homeowners who can’t make their payments. This entails a means test, so one should be created. If the homeowner still can’t pay the mortgage, then the term of the loan should be extended and the interest rate reduced. The federal government can compensate the lender for any loss.

That would direct relief to those who need it most.

Would there be complaints by those not facing foreclosure because the means test demonstrated their ability to pay? Would they be jealous of those who received assistance when they did not? Perhaps. But it would still be worth it to stop the losses and halt the foreclosures.

Would prices stop falling? Probably not. But they would not fall as far as they will fall if we don’t stop the foreclosures.

Washington should stop thinking small!

© 2008 Michael B. Lehmann

Friday, November 7, 2008

Minus 1.2 Million, And Counting

THE BE YOUR OWN ECONOMIST ® BLOG

The Lehmann Letter ©

This morning’s employment report was remarkable (http://stats.bls.gov/news.release/empsit.nr0.htm). It began:

“Nonfarm payroll employment fell by 240,000 in October, and the unemployment rate rose from 6.1 to 6.5 percent, the Bureau of Labor Statistics of the U.S. Department of Labor reported today. October's drop in payroll employment followed declines of 127,000 in August and 284,000 in September, as revised. Employment has fallen by 1.2 million in the first 10 months of 2008; over half of the decrease has occurred in the past 3 months. In October, job losses continued in manufacturing, construction, and several service-providing industries. Health care and mining continued to add jobs.”

We lost 240,000 jobs last month and September’s loss was revised upward to 284,000. Moreover, we’ve lost 1.2 million jobs this year, for an average monthly loss of 120,000. That’s awful.

If you update the chart below in your mind’s eye, you can see that the recent monthly losses of 284,000 and 240,000 are as bad as the 2001 dot-com recession. And all signs seem to say: The worst is yet to come.

Job Growth

(Click on chart to enlarge)

© 2008 Michael B. Lehmann

The Lehmann Letter ©

This morning’s employment report was remarkable (http://stats.bls.gov/news.release/empsit.nr0.htm). It began:

“Nonfarm payroll employment fell by 240,000 in October, and the unemployment rate rose from 6.1 to 6.5 percent, the Bureau of Labor Statistics of the U.S. Department of Labor reported today. October's drop in payroll employment followed declines of 127,000 in August and 284,000 in September, as revised. Employment has fallen by 1.2 million in the first 10 months of 2008; over half of the decrease has occurred in the past 3 months. In October, job losses continued in manufacturing, construction, and several service-providing industries. Health care and mining continued to add jobs.”

We lost 240,000 jobs last month and September’s loss was revised upward to 284,000. Moreover, we’ve lost 1.2 million jobs this year, for an average monthly loss of 120,000. That’s awful.

If you update the chart below in your mind’s eye, you can see that the recent monthly losses of 284,000 and 240,000 are as bad as the 2001 dot-com recession. And all signs seem to say: The worst is yet to come.

Job Growth

(Click on chart to enlarge)

Recessions shaded

The chart was taken from http://www.beyourowneconomist.com. [Click on Seminars and then Charts.] Go there for additional charts on the economy and a list of economic indicators.)

The chart was taken from http://www.beyourowneconomist.com. [Click on Seminars and then Charts.] Go there for additional charts on the economy and a list of economic indicators.)

© 2008 Michael B. Lehmann

Wednesday, November 5, 2008

The New President’s Dilemma

THE BE YOUR OWN ECONOMIST ® BLOG

The Lehmann Letter ©

President-elect Barack Obama faces a dilemma.

A severe recession is unfolding. Demand, production, employment, income – all are falling and falling hard. The new president has two traditional remedies at his disposal: Reduce taxes so that consumers can purchase more, thereby stimulating production and employment, or increase public-works spending to directly boost employment. These remedies will, of course, raise the federal deficit.

Therein lies the dilemma: The president can not effectively deal with the recession and shrink the deficit. Which horn of the dilemma should the president choose? Fight the recession or deal with the deficit?